When I was a child, my parents taught me not to lie due to the moral and social problems that lying creates. Lying misinforms the people you’re talking to about both the subject you’re talking about and the fundamental nature of your character, while discoloring future information you provide and weakening the counsel that you give. Lies are also extremely brittle, with each repetition of the lie usually requiring a new lie to go with it to sustain the narrative of the original lie. Lies don’t even have to be straightforward - you can leave information out, you can tell a partial truth, or you can wrap a lie in truths to legitimize it.

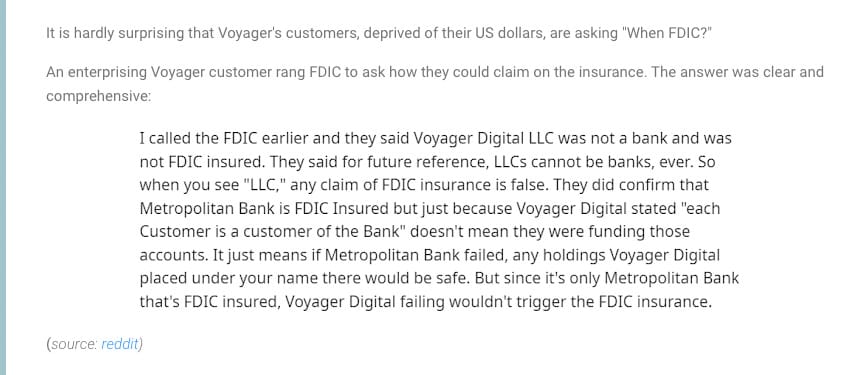

For example, Voyager, a publicly-traded crypto lender that has suspended all trading and withdrawals as of July 1, claimed that customers were given FDIC insurance on their balances (up to $250,000) in the event of some sort of insolvency on the part of Voyager itself. Except it’s become clear, as noted by writer Frances Coppola, that Voyager has an omnibus account at Metropolitan Bank for all client funds - an account which is FDIC insured - except this isn’t how FDIC insurance works:

To quote Coppola:

The omnibus account at Metropolitan Commercial Bank comes with FDIC insurance of up to $250,000. This protects the money in that account from loss in the event of the bank's failure. It does not protect Voyager's customers from losses in the event of Voyager's failure. This is clearly stated in Voyager's own customer service agreement.

Furthermore, Voyager has claimed in its terms and conditions that all movements in and out of the omnibus account are controlled by the bank itself on behalf of customers:

Now, this is odd. If movements in and out of the account are controlled entirely by the bank on behalf of Voyager's customers, then Voyager should not be able to suspend US dollar withdrawals. But it has. Clearly, therefore, Voyager is controlling access to the money, despite its statement that it does not provide "any services pertaining to the movement of, and holding of, USD".

Coppola’s question is very reasonable: if Voyager does not move, or touch, or do anything with customers’ funds, why are withdrawals frozen? The FDIC insurance question is also incredibly thorny, because, as Coppola explains, they have failed to act as a fiduciary or agent for its customers’ US deposits, nor does it appear to have segregated these funds from the rest of their funds. In fact, FDIC insurance protects entirely against the failure of a bank (which Voyager is not), and the funds in the omnibus account are protected up to $250,000 total, not per customer.

And, to be 100% clear, FDIC insurance is something given to a bank, not a bank’s customer. And cryptocurrency companies have been lax to get bank charters because there are all these annoying “rules” and “regulations” you “have to follow otherwise you go to jail.”

Voyager is also a victim of the fallout of massive crypto hedgefund 3 Arrows Capital, who have now filed for Chapter 15 Bankruptcy after their strategy of “I hope nothing and ever happens to me!” failed. By “victim,” I mean that 58% of the loans that Voyager has issued have been to 3AC, and its loan book is 50% of its total assets. They will likely never see a dime of the $660 million they loaned 3AC.

In very simple terms, Voyager lied to customers about whether their funds were insured as a means of conning them into investing with Voyager. At the same time, Voyager issued loans to hedge funds like 3 Arrows Capital, assuming that nothing bad would ever happen to them, Voyager, or the crypto markets. While it’s not obvious exactly what underwriting went into these loans, my technical assessment is “it wasn’t enough” because they loaned hundreds of millions of dollars to them based on what appears to be the assumption that nothing bad was ever going to happen.

In plain English, 3 Arrows Capital borrowed cryptocurrency from many places based on its history of otherwise being good at guessing when the number would go up. The people lending them the money also agreed that the number would never go down or up in a way that 3 Arrows Capital would dislike and thus chose to lend them incredible amounts of money, betting, as lenders do, that they would not lose all of that money in its entirety. BlockFi, another “I guess this is kind of a Ponzi scheme” crypto loan company, claimed that a “large client failed to meet its obligations on an overcollateralized margin loan,” and that client has turned out to be 3 Arrows Capital, and that the loan was for a billion dollars. Singapore’s regulator has claimed that 3AC was “providing misleading information” to clients.

What may be becoming obvious to some of you is that the crypto industry was built off the back of everybody writing poorly-collateralized and poorly-underwritten loans for incredibly large amounts of money. Based on further analysis, traditional financial institutions weren’t offering this “because the loans were incredibly fucking stupid, and the people loaning the money did not appear to abide by any kind of fiduciary sense.” Crypto lenders have been lending money to other companies so that they can take loans out with other crypto lenders and then use the profits from those loans to invest in more loans with more companies. When these loans fell through, or the time came for further collateral, these companies scrambled to sell off assets like Bitcoin or Ethereum to cover these losses, putting massive sell pressure on the crypto market.

And, as Coppola suggests, Voyager may have paused withdrawals because they used customer funds to cover their losses:

This brings us back to Voyager's enormous cash burn over the last nine months. "Cash held for customers" is supposed to be segregated, but as it's on Voyager's own balance sheet this is merely an accounting fiction. There's nothing to stop Voyager borrowing its customers' dollars. So, what if Voyager has used the omnibus account as a source of dollar liquidity? What if it has drained that account to defray its exorbitant operating expenses, and now can't put the money back? Indeed, what if all along it has funded that account on a just-in-time basis, borrowing US dollars when needed to meet withdrawal requests, and now it can't fund it any more because its credit lines have been pulled? This would explain why it has had to suspend US dollar withdrawals. It can't pay out money it doesn't have and can't get.

While it’s not confirmed, it seems worryingly likely that customers - as ever - are the real victims of the hubris and idiocy of a massive cryptocurrency disaster. While a kinder person may argue that 3AC pulled the wool over their eyes, nobody appears to have asked the simple question: why can we not get loans like these from traditional banks? And why are these banks also not issuing these loans to 3 Arrows Capital themselves? If the answer is “because the legacy banks ask too much,” then perhaps that’s a sign to not loan anyone that much money.

Now, you may ask why the cryptocurrency industry would engage in such reckless activity, and the answer is “because it sort of worked before.” When things were going well, these massive loans were extremely profitable for both sides, collateralized through massive purchases of cryptocurrency (thus sending the market upwards in the process). And when those loans ended up making more money, that money was put right back into more cryptocurrency, invariably being used to invest in more loans.

Sidenote: referring to this a house of cards is insulting to cards, which have a consistent value and utility, unlike cryptocurrency.

They also, I believe, do not really care. The people making these decisions are already rich, and because of a lack of regulation, they will likely escape any real consequences. They may get fined, they may get humiliated, but they will find solace in the fact that they have unimaginable wealth obtained through quasi-legal means. They have willingly endangered millions of people’s money because they could, and they will likely get away with doing so.

The Vibes of Vultures

Despite claiming to be the antithesis of the classically elite-driven financial markets, cryptocurrency has become an altogether worse system where the poorest and most exploited treat the rich and powerful as precious darlings that must be protected. Business Insider's Kari McMahon reported on the existence of “directors of vibes” in crypto companies, which she charitably describes as a hybrid role of customer success and corporate culture, but more accurately as “snake oil salesmen.”

Let’s check out what this term supposedly means:

For Deeze, day-to-day vibe management goes from attending internal sync ups, having external meetings with artists and curators and running Twitter spaces for the community.

…

For ashh_eth, who's real name is Asher Hoffman, it's a lot more about maintaining the vibes on the Discord servers for both the DeeKay and Random Character Collective projects where he works as chief vibes officer.

"My positions are similar in the sense that I am there to help cultivate the community and make sure that not only the vibes are good, but everybody's having fun and feels welcome," Hoffman said.

The correct term for this nebulous role is ‘evangelist,’ or ‘judas goat.’ These people are con-artists, working for con-artists, helping con people by telling them that things will be alright when “alright” is dictated by the whims of the ultra-rich people controlling the industry. If you require a role to “make people feel better about the markets,” and you do not control the markets, all you are doing is trying to convince people to invest in (or not exit) a market so that you don’t lose money. While the same could be said of many other roles, in the case of cryptocurrency, these people exist entirely to keep people from leaving the system. They are unlicensed therapists with the worst possible agenda - propping up the interests of rich people that have constructed a system where they profit almost entirely from exploiting those under them.

McMahon’s piece is frustrating because (like so many cryptocurrency articles) it fails to interrogate a single part of the industry. These are crisis communicators, except unlike most companies and their crises, there is no substance to communicate, no fundamentals to draw on, no cause and effect that a person can follow from having their “vibe” adjusted. These are not “vibe” officers, but Chief Manipulators, peddling half-truths that resemble explanations to people desperate to believe that things are not as bad as they seem. These roles have grown in a bear market because the number isn’t going up, and cryptocurrency sites keep locking up people’s funds, and saying “WAGMI” isn’t quite cutting it.

This is a great time to say that if cryptocurrency had a real utility or purpose, there would be no need for a “director of vibes.” There is no need for a Business Insider article about a job that mostly appears to be posting memes and being saccharine as the world falls apart:

“Bad vibes” in this case refers to “actual, real stuff that is bad that is happening right now,” also known as “the truth.” Anthony Pompliano posting that “you’re in charge of your own happiness” disregards the fact that his work evangelizing cryptocurrency and suggesting that there is a method to the madness beyond “legalized insider trading” and puts the responsibility on the people that he’s helped con. These “vibe officers” exist to trick people into believing there are moral and philosophical underpinnings to success, and that this is a situation that can be handled by thinking good thoughts. Now cryptocurrency has switched doctrine from “you are the chosen ones for believing” to saying things about “not being distracted” or “focusing on building”:

Except, in the most painful irony available, this is exactly the same kind of nebulous capitalist bullshit that every single rich and famous person tells themselves is the reason that they succeeded. It is not simply enough to “do what it takes” - one does not become rich or successful in cryptocurrency (or America) just because they “worked hard.” Pompliano got rich because he was able to afford to invest in Bitcoin when it was lower than it is now, and because he had the funds to take that risk at the time. One cannot simply “work hard” to get out of the hole they’re in if their assets are frozen in Voyager, or if their investment in Luna went to $0, or if their margin calls got obliterated. One cannot simply “do what it takes” when “what it takes” means “have the right connections and be party to deals that the public doesn’t have access to.”

These are the same nebulous lies told by every single celebrity investor or entrepreneur. And these are the lies of the old rich, told by the new rich and sold to the current and future poor.