Thanks for reading this week’s free Where’s Your Ed At newsletter. As I said last week, I’m taking the rest of this week off, so there won’t be a premium on Friday. That said, if you aren’t already a member, now’s a great time to subscribe.

To celebrate the one year anniversary of the premium newsletter, I’m offering a sale on one-year subscriptions. Between now and midnight July 22, you can get a permanent annual rate of just $60— a $10 discount on the usual price of $70 - for life. Click here for the offer.

In addition to getting access to the entire back catalog of premium posts, you’ll also receive one additional post each week — usually anywhere between 10,000 and 20,000 words — covering the most pressing topics in the AI bubble - the best value in tech analysis. Highlights include last week's Hater's Guide To The Memory Crisis - a guide to how AI made everything more expensive - How OpenAI Kills Oracle (which pairs nicely with the Hater's Guide To Oracle), The Hater's Guide To NVIDIA, The Hater's Guides To Private Credit and Private Equity, and how the entire AI Compute Demand Story Is A Lie.

Today’s piece is one of the largest free newsletters I’ve ever written, and pulls together the last six months of my work.

And it all starts with a question: how much do you trust Sam Altman? The stock market and (to some extent) the global economy rests on your answer.

You see, OpenAI has become one of the largest liabilities in recent economic history. You can argue that OpenAI’s no longer the focal point of the AI bubble — you can talk all you want about open source models or Anthropic or any number of other elements — but without OpenAI, the AI industry doesn’t exist, and the justification for trillions of dollars of capex evaporates.

The AI bubble isn’t a result of any actual return on investment — whether that be in purely monetary terms, like revenue or profitability , productivity gains, or anything tangible or measurable. Rather, it’s an episode of cult-like psychosis that infected the brains of some of the most powerful and wealthy individuals and institutions, where the powerful mythology of a company inspired — and been used to inspire — the greatest capital misallocation in history.

As much as this’ll piss some people off, I fully believe that the only reason this has kept going so long is that OpenAI has yet to collapse. Its failure would be a watershed moment — the Lehman Brothers of the AI bubble, and an event that would define the end of one epoch, the start of another, and that would shake the afflicted out of that psychosis. Absent this wake-up call, NVIDIA has continued to sell GPUs, the coffers of the semiconductor industry have continued to swell, and more and more spending commitments have been made.

Look. OpenAI intends to burn over $852 billion by the end of 2030. It accounts for $748 billion of the remaining performance obligations of Microsoft, Amazon, and Oracle, on top of at least another $70 billion of RPOs across Cerebras, CoreWeave, Nebius, IREN, Lambda, and Nscale (per Kakashii), and plans to spend indeterminate billions’-worth of Broadcom “Jalapeno” chips. It intends to spend $50 billion or more on compute this year, which I estimate is more than 50% of all global AI compute spend (with OpenAI taking up 50%+ of all AI compute infrastructure).

OpenAI can only afford to pay that as a result of its latest (assuming it fully closes) $122 billion funding round, of which it has received at least $50 billion, with $20 billion from SoftBank (of $30 billion, with the third tranche due October 1, 2026). NVIDIA mentioned in its latest quarterly earnings report that it “estimate[d] that one AI research and deployment company contributed to a meaningful amount of [its] revenue by purchasing cloud services from [its] customers in the first quarter of fiscal year 2027,” referring, of course, to OpenAI.

The AI Bubble Is An OpenAI Bubble — To A Mortal End

OpenAI is the reason anyone cares about AI. In March 2019 (per JustDario), NVIDIA bought a company called Mellanox that made the high-speed networking tech necessary to create AI GPU clusters, and four months after that, Microsoft invested a billion dollars in OpenAI and started buying AI GPUs and building AI infrastructure for it. By March 2020, NVIDIA would ship its A100 GPU, and in May 2020, Microsoft would announce it had built a supercomputer just for OpenAI with “more than 285,000 CPU cores [and] 10,000 GPUs.”

The launch of ChatGPT in November 2022 came at the perfect time for a tech industry that had run out of ideas and was flirting with a prolonged depression. The IPO market had collapsed, interest hikes killed the Zero Interest Free era dead, pandemic era overhiring began to unwind with some of the worst layoffs in the history of the industry, global venture funding dwindled after historic overinvestment in 2021, and tech stocks took a massive beating.

For the first time, the tech industry was forced to cut its cloth in accordance with its means — something which it has historically been loath to do. Big tech was unpopular, both with investors and the general public. The excesses of the past decade — combined with the growing frustration with, for lack of a better word, “tech exceptionalism,” where it believed that the rules which governed the rest of the world didn’t apply to Silicon Valley — had tested the patience of both regulators and lawmakers. And, in the absence of “one more thing” — a big, splashy, game-changing product category — it no longer had an excuse for its prodigal spending, or its regular breaking of the rules, both written and unwritten, that govern society.

The existence of OpenAI justified an era of mania and opulence. Hyperscalers, bereft of new hypergrowth ideas, were able to point at the fact that ChatGPT had “the fastest growing userbase of all time” and the Microsoft “supercomputer” that built it and tell their investors that if they didn’t invest, they’d be left behind, with Amazon, Meta, and Google announcing their own nebulous “supercomputers” in 2023.

By the end of 2023, NVIDIA had sold 500,000 A100 GPUs, and the only reason it did so was because of ChatGPT’s rapid growth. Sam Altman’s brief ouster only sought to inflate the AI bubble by adding a layer of dull palace intrigue to a tech industry bereft of whimsy or character — and helped further entrench Microsoft’s role as the paternalistic benefactor of OpenAI, which made sure that Altman returned to the helm.

To be clear, when I say “rapid growth,” I mean that OpenAI hit 100 million weekly active users by the end of 2023 and had about $108 million in monthly revenue. Microsoft would invest $10 billion more that year, with the majority of that funding coming in the form of credits to be used on Microsoft Azure.

OpenAI is also the reason that Anthropic exists — not just because multiple founders came from the company, but because both Google and Amazon both agreed to give it a total of $6 billion in 2023 as a means of “competing” with Microsoft’s new obsession, which allowed both to justify spending further hundreds of billions of dollars “to make sure they didn’t miss out on AI.”

When you remove the term “AI” from the equation, this all seems a little ludicrous. $16 billion in equity investment on top of what was, by the end of 2023, over $150 billion in capital expenditures, all of which was pretty much justified by the fact that a single website had been very popular.

And the only reason either of these companies were able to grow was because of hyperscalers bankrolling their entire infrastructure.

In the fourth quarter of 2023, global venture capital funding had dropped to its lowest levels since the third quarter of 2016, with American startups taking up $183.6 billion of the year’s investments. Venture capital alone couldn’t have — and wouldn’t have — actually backed OpenAI or Anthropic at the scale that was necessary to build their infrastructure, nor would there have been any of the hunger from hyperscalers or those providing debt for data centers without hyperscalers inflating both of these companies, almost entirely because of the success of OpenAI.

Remove OpenAI from the years 2020 through 2024 and the AI bubble wouldn’t have inflated at all. No other major AI companies showed any sign of life — not those peddled by hyperscalers, funded by venture capitalists, or those launched by other tech firms.

The only reason that any hyperscaler AI efforts have any revenue — and outside OpenAI and Anthropic it’s pretty meager! — is because they knew they could just sit there and keep saying “AI is the future” until their customers eventually gave in and tried it…largely because everybody was talking about ChatGPT.

Anthropic was considered an also-ran until early 2025, and only continued to get funded because people wanted to invest in the next OpenAI, and Anthropic’s initial funding rounds and infrastructure buildout were only justified in terms of competing with OpenAI.

Those $178.5 billion in US-based data center debt deals in 2025? Pretty much entirely justified by the growth of OpenAI and its rapacious hunger for compute, because outside of OpenAI (and eventually Anthropic), nobody else was using massive clusters of tens of thousands of GPUs, nor does a market for compute at that scale appeared to have popped up in the months and years since.

The largest consumers of compute remain Microsoft (for OpenAI), Google (for Anthropic), Amazon (for OpenAI and Anthropic), CoreWeave (for OpenAI and Anthropic), Meta (which is copying what the other hyperscalers are doing), and Oracle (for OpenAI). Otherwise, there’s very little evidence — and boy, have I looked — that there’s more than a few billion in demand for AI compute, and that’s being generous.

All of those investments — both in AI startups and data centers — existed to fund either the next OpenAI or become the next OpenAI’s landlord.

The assumption — because nobody ever thinks things through — was that because one OpenAI existed, many OpenAIs would bloom. That because one large customer of compute existed, the template had been built for future compute-intensive startups…and, again, because nobody ever thinks about anything, nobody ever stopped to realize that the reason there isn’t another OpenAI is because OpenAI and Anthropic are financial psy-ops by the largest software companies in the world.

OpenAI and Anthropic Are Hyperscaler Psy-Ops Built For The Monoculture of Silicon Valley

The grim truth is that you can’t venture fund an AI lab. While OpenAI and Anthropic have raised nearly $300 billion in the last few years, their actual infrastructure costs — the GPUs and the data centers to power their services — were entirely funded by hyperscalers, likely costing another $250 billion in the process, given that Microsoft has said it spent $100 billion on its OpenAI relationship as of early 2026.

Yet the real cost wasn’t just financial, but the experience and industrial know-how to actually execute on a massive infrastructure bailout. Other than Google, Microsoft, and Amazon, nobody else has the scale or experience to build the kind of AI clusters that OpenAI (and eventually Anthropic) needed.

We know that for a couple of reasons. First, because prior to 2023, there were few — if any — companies actually building AI computing clusters at the kind of scale demanded by OpenAI or Anthropic. The closest thing that one could point to were crypto-mining firms, and it’s telling that many of the neoclouds today (most famously Coreweave) started life running warehouses full of ASICs to mine Bitcoin and Ethereum.

Second, because, based on conversations with people in the data center industry, the whole Overton window of what is considered to be a “big” facility has shifted. Previously, a 50MW data center would have been considered a significant (even noteworthy) development. These were the exception, and not the rule, with most data centers being vastly more modest affairs. The only companies which had any experience building at that scale were, for the most part, hyperscalers.

By treating OpenAI as a “venture backed startup,” hyperscalers created the illusion that this was the next type of big company that would in turn create the next great demand center in cloud computing, except the only reason that these companies existed was because of the hyperscalers themselves willing them into existence, funding them with incredible sums, and allowing them to burn as much money as they’d like.

This is why the idea that OpenAI will continue to grow infinitely is central to the mythology of the AI bubble. The existence of one OpenAI allows others to — no matter how illogical — imagine the existence of more OpenAIs, which in turn means that those OpenAIs will need just as much compute as OpenAI.

The dimwitted investor who believes this tripe can justify it through any number of different buy-side analysts or captured members of the media that talk about the “insatiable demand for compute,” pointing to capacity constraints (caused by slow data center construction and — hah! — OpenAI and Anthropic taking up much of the world’s compute) and increasing GPU prices as proof that actually, there’s tons of demand, all without ever really thinking too hard.

The greatest trick that hyperscalers played was never backing down. By sinking more than a trillion dollars into AI capex without ever showing a single dollar of profit, they justified literally anyone investing in AI data centers under the logic that “the largest companies in the world couldn’t be wrong,” even if the reason they were doing so was to expand capacity for OpenAI and Anthropic, who the hyperscalers themselves incubated.

It is fundamentally illogical and insane for hyperscalers to have spent so much money on AI infrastructure, and the reason that few people will say so is because it was, until recently, considered radical to suggest that this was a waste of money, almost entirely because of the existence and continued growth of OpenAI.

Sidenote: while I realize Anthropic has taken up a lot of attention and grown rapidly in the last year, it’s only been able to do so A) because of the mythology of OpenAI and B) because it too was incubated and allowed to run at a massive loss too.

Whatever utility you may or may not get out of LLMs is irrelevant because it has not, for the most part, been what actually underpins data center investment. While accelerating gains in code generation (itself something that could have only happened without vast subsidies) might have helped grow Anthropic, the vast majority of data center capex has been built chasing the dragon of what AI could be rather than any connection to the revenues or economics of the companies at large — outside, of course, their compute spend.

This is the underlying greed that has driven this wasteful, reckless and destructive era — the belief that there will be another OpenAI and, as I’ve said, the chance to become the next OpenAI’s landlord. And because the media and analysts very rarely have original ideas, everybody justified (and justifies) the waste through the same tired mantras, saying it was “just like Uber (nope!)” or “just like Amazon Web Services (between 2003 and 2015, Amazon spent $29.7 billion on capex, normalized for inflation).”

And like any great investment bubble, the more money that piled in, the greater the fear of missing out, the more dollars that can be justified in turn, and the more-complex and deranged the mythology becomes, which is why you have noted venture capitalists claiming that AI labs have “90%+ inference margins,” a completely unproven statement that AI boosters cling to and repeat often enough that it’s taken as gospel, likely to avoid thinking about the fact that you can burn $14,000 in tokens on a $200-a-month ChatGPT subscription.

This kind of mythology only grows in an environment deliberately deprived of good information. The fact that we’re four years into this horrible bubble and still don’t have consistently-held consensus around the actual costs of large language models is a testament to an industry-wide effort to suppress them.

OpenAI, Anthropic, Microsoft, Google, and Amazon have done everything in their power — based on discussions with sources familiar with their infrastructure — to obfuscate the actual underlying costs of their operations, and Silicon Valley, an industry of alleged free thinkers and individuals, is more than willing to accept whatever convenient myths might sustain their dreams.

And in the end, they all became useful idiots for hyperscalers. Their obsessive attachment to OpenAI — and by extension Anthropic — seems like a decision made under the auspices of “democratizing powerful AI,” all as effectively every dollar flows to either Microsoft, Google, Amazon, or Oracle, who in turn feed that money to NVIDIA or Broadcom, who in turn feeds that money to TSMC, SK Hynix, Samsung, or Micron.

Invest in an AI startup? They’re gonna be paying one of the AI labs, who will in turn pay a hyperscaler. Invest in an AI infrastructure company? That money will flow to NVIDIA, and then upstream to semiconductor companies. In the end, whether they die or get acquired (as none of them are going public), all of the value will end up in the hands of one of the hyperscalers who created this imaginary era, then helped inflate it into something very, very dangerous.

Why The AI Bubble Can’t Survive Without OpenAI

Yet the problem is that this industry cannot, under any circumstances, survive without OpenAI.

When people discuss OpenAI’s potential collapse, they act with pure cowardice either saying “it won’t be that bad” or say something vague about it “being too big to fail.”

If OpenAI — the company with the most money and the most infrastructure and the most attention and the most talent in AI — collapses, it will likely do so after AI data center debt and venture capital funding has been almost entirely exhausted.

You see, Goldman Sachs’ Jeffrey Papai recently noted that it will be “very difficult” to replicate the hundreds of billions of dollars that hyperscalers have raised in the last four years — $244 billion in 2026 alone if you include NVIDIA and SpaceX — which is a problem considering that they can no longer fund their data center capex using their cashflows as of Q3 2026.

And to be clear, hyperscaler capex doesn’t have to stop for NVIDIA to stumble. It just has to slow down meaningfully enough that Jensen Huang can no longer give investors 60%+ year-over-year revenue bumps, because the AI bubble is built on vibes, and it can only survive so long as those vibes don’t become sour.

Yes, yes, I realize there are other customers, but the vast majority of NVIDIA’s demand comes from hyperscalers, who are (for the most part) either building out their operations for OpenAI and Anthropic or simply copying what the other hyperscalers are doing (see: Meta and SpaceX).

Once hyperscalers stop spending money, banks that are afraid of “choking” on data center debt will see that a vast amount of capital is leaving the market and underwrite (or not, as the case may be) deals as such.

This will mean, at some point, that both OpenAI and Anthropic will be walking around with their hands out saying “money please!” at precisely the moment that everybody will be cutting back. While NVIDIA might get a little desperate and throw some extra cash their way, if revenues start collapsing, so too will its interest in further inflating the bubble as investors begin to ask whether any of this was real or one large circular financing scam.

While this is absolutely a problem for Anthropic — especially after its $35 billion debt deal with Broadcom — it’s much, much worse for OpenAI, which has (as mentioned) made $748 billion in compute commitments to some of the largest and well-lawyered companies in the world. OpenAI’s continued marketing efforts involve constantly refreshing rate limits around the launches of its most-expensive models, giving away millions of dollars of tokens to startups, and generally running the “grow as fast as possible and work out a business later” model into the ground at speed, all fueled and funded by Clammy Sammy Altman’s nasty habit of overpromising and underdelivering.

Clamuel’s biggest mistake was leaving the pearly gates of the hyperscalers and dancing with the mortals of Oracle, Cerebras, and CoreWeave. While Microsoft or Amazon might be willing to extend payment terms as a means of saving face and prolonging the inevitable, Oracle — a law firm with a software company attached — is more than capable of loud and aggressive litigation under any contractual breach.

Then there’s the fact that Apple is suing OpenAI after poaching multiple engineers for its hardware efforts and allegedly both coaching and coercing them into stealing trade secrets, which is all but certain to destroy any chance of OpenAI releasing a device in the next few years…and potentially the company itself. These are extremely serious allegations, with Apple also accusing OpenAI of trying to coerce trusted partners into revealing manufacturing techniques for iPhones — the kind of thing that can (and will) lead to brutal discovery and potentially criminal charges.

OpenAI also, as I’ve mentioned, needs to keep growing to keep up with those bills, and at some point will run out of real dollars to pay people, likely at exactly the time that it’s hardest to find more of them. While there might be billions of dollars left to be raised, to pay any of its bills, OpenAI needs tens of billions of dollars multiple times a year. Based on my own reporting on its audited financials from 2024 and 2025, OpenAI will need to raise funding at least three more times in the next decade.

To make matters worse, its free users have become a massive liability. While The Information reported that OpenAI expected to generate $2.4 billion in ad revenue in 2026, and $102 billion in 2030, it turns out that reality is a little harsher, with analyst eMarketer projects that the entire AI chatbot ad industry combined will only make $1 billion this year, with the entire market making $5.41 billion by 2030.

This means that the 900 million weekly active users of ChatGPT will remain a massive drain on the company’s finances, with only 5% or so of them opting to pay, and a projected 80% of its $20-a-month users expected to churn in 2026.

At some point, OpenAI will simply run out of money. It’s nearly exhausted every available source of capital, and now that it’s likely delaying its IPO to 2027 — largely in part because it couldn’t list at a $1 trillion valuation — it will have to raise again, potentially at a down-round valuation or at a modest increase which will, in turn, make it much more difficult for investors to see a return in an IPO.

Investors will likely ask questions like “why couldn’t you go public?” and “what is it that bankers didn’t like?” as Sam Altman looks at them like this:

You see, OpenAI is awesome at selling mythology and hype, but crumbles the second that its numbers have to face the cold, harsh light of day.

While it’s been able to skate by in situations like Altman’s ouster and its conversion to a for-profit, these were strictly legal situations that could be dealt with by lawyers and cheered on by the press. OpenAI has never faced a problem like “not being able to pay its bills” or “breaching a contract with a major company,” and I think these are an inevitability in its future.

Sidenote: Yes, yes, you’re going to say “buhhh, bailout (nope!),” but even if Trump were to funnel another $42 billion to OpenAI, it wouldn’t cover a year’s worth of compute in 2027, the year that I imagine the Hellmouth opens and swallows it whole. If your argument is that OpenAI is going to get nationalized or “the military funds it indefinitely,” you are catastrophizing as a means of pretending you have control over the future in a way that feels intellectually satisfying, all without any of the messy work of interacting with the horrors of reality.

In the end, OpenAI’s collapse will be a dramatic narration of the boring, horrifying economics of the AI bubble.

Let me explain:

- OpenAI’s collapse will be a direct result of its loss-laden economics — its doomed, loss-making subscriptions, its pathetic advertising revenue, and API costs that became a “huge issue” for its enterprise customers — and the fact that outside of the hype, AI lacks measurable ROI.

- When OpenAI eventually leaves CoreWeave, Cerebras, and Oracle in the lurch, there won’t be anyone else to pick up that compute.These are all debt-laden companies, and without meaningful revenues, they’ll struggle to service their obligations.

- When OpenAI dies — likely folding into Microsoft in the process — it will massively pull back on any and all compute demands, with the likely end of and free ChatGPT and a massive price bump across the board.

- OpenAI’s demise would also naturally call into question the rationality of investing in any AI startup. If the largest, best-funded, best-resourced company in the entire industry backed by the world’s largest software companies couldn’t make it, why would you believe somebody else would do so?

- The collapse of the largest company in the ecosystem would also seize up any and all AI data center debt (if any exists at that point), because the literal largest consumer of AI compute would be dead.

The AI bubble is inflated based on hype and hopium rather than tangible proof or substantial revenues driven to anyone outside of the semiconductor industry, and without NVIDIA’s massive returns, I don’t think anybody would’ve taken it seriously past 2024. Any and all achievements of the AI industry are a direct result of market psychosis, a broken media ecosystem, and a trillion dollars that could’ve been sunk into literally anything else, and must be evaluated as such.

The double-edge sword of a mythology-inflated bubble is that it’s much harder to sustain when said mythology dies. The AI bubble was able to grow to such a horrendous size because the markets and the media were willing to accept basically anything that Sam Altman or the greater AI industry said.

By waving away any economic problems as growing pains and dismiss those who would scrutinize it as haters or cynics, reporters and analysts provided investors with the justification to invest again and again in these companies without them ever having to make a real business, which means that, well…they don’t have real businesses, which is a problem when you need to actually pay somebody money that wasn’t given to you by a venture capitalist.

This will leave the AI industry short-changed in its most-desperate times.

The media is important for many, many reasons, but one of the biggest ones is that scrutiny is what keeps capital in check, for the benefit of humanity and at times the companies themselves. By choosing to pull their punches, ignore glaring economic problems and accept every projection with blind faith, the media empowers grifting and suffocates good businesses as a result, encouraging bad behavior and helping them raise unbelievable amounts of money at ridiculous valuations without worrying about having to make a good business. In some cases, the media even encourages them to do so, saying that “all startups lose money at first” instead of thinking about things for a fucking second.

When companies know they won’t face that scrutiny, they engineer themselves as such, putting off ever finding a real business model in favor of whatever will make them buzzy enough to get coverage and raise funding as a result. In a vacuum of skepticism, bubbles inflate, monsters get rich, and regular people always get left holding the bag. As a result, if companies ever bother to become a real business, they only do so at the very last minute, endangering anyone who has backed them and every counterparty in the event they’re incorrect.

When OpenAI dies, it will be after a prolonged period of desperate reorganization and attempts to appeal to investors and the media that it can, in fact, become a real business. These attempts — price increases, price cuts, selling off IP, nebulous circular deals, and so on — will all fail, and by the end, Sam Altman will have run through every single trick imaginable to keep the party going.

And when those fail, what do you think Perplexity does? How about Harvey? Cursor got the last chopper out of ‘Nam with the SpaceX acquisition (assuming it actually happens), but what, exactly, is Cognition, or Glean, or Sierra, or really any AI startup meant to say to compel investors to believe in them once OpenAI dies? That they’re different? That they’re gonna work it out after the company that got given basically everything it needed failed?

The entire AI industry’s sales pitch is that OpenAI opened the world’s eyes to the power of AI, and that giving the AI industry as much money as possible would end in economic abundance the likes of which we’ve never seen. Instead, we’ve got two AI labs that both lose billions of dollars, and the latest model from one of them randomly deletes people’s stuff.

It’s not like any of this was sold on actual ROI or real businesses or returns or productivity or any actual measurable thing other than physical infrastructure erected in its honor.

There are simply no compelling stories about the AI industry that can be told in the present tense. Everything is always based on the theoretical multiplicative power of just waiting a few more years, which becomes much harder to believe if the company with the Mandate of Heaven gets sent to Cocytus.

This will have massive downstream effects on basically everything and everyone connected to the AI industry. You won’t be able to raise money for a startup to spend money on compute, nor will you be able to convince somebody that your LLM wrapper will change the world, nor will you be able to justify a massive valuation. Venture capitalists fancy themselves as brave soldiers of the economy, but are really cowardly lemmings that will sprint for cover the second that things get rough.

Why Anthropic Is In A Very Similar Situation To OpenAI

I also keep hearing from people that Anthropic is magically safe from the AI bubble’s clutches, or insulated from its rotten economics. The amount of pure mythology and misinformation I read about this company on Twitter is genuinely offensive, and the fact that journalists have categorically failed to push back against it is proof that too few people give a shit about anything other than which boot they get to lick next.

Anthropic faces the same economic realities as OpenAI. It burns billions of dollars on training, it hides inference costs in sales and marketing, and the only real differences are that it focused more on coding and made fewer ridiculous infrastructure commitments…right up until this year, when it committed $200 billion in compute and hardware commitments to Google, raised $35 billion in debt from Apollo to buy Google TPUs, signed a $15 billion a year compute deal with SpaceX, and agreed to a 20-year-long, $19 billion lease with TeraWulf.

Much like OpenAI, Anthropic is also doing way, way too much. There’s Claude for Life Sciences, Claude for Legal, Claude for Small Business, Claude Design, and even, for whatever reason, reports that Anthropic intends to develop its own drugs — and instead of saying “hey man, what the fuck are you doing?” the media falls over itself to repeat and celebrate every single one as if they’re all viable or useful products. Anthropic is as messy, disorderly and unfocused as OpenAI, but has done a better job of convincing people that it’s somehow “ethical” as it fucks over its partners and farts out 200 new products a month.

This is a company that lacks focus or vision other than “more” and “bigger.” The only thing that differentiates OpenAI from Anthropic at this point is the nebulous promises of “AI code” and Dario Amodei’s Doom Trolling and safety theater.

The fact that the majority of the media made no efforts to push back against its shenanigan-rich “profitability” narrative is why we’re in this fucking mess.

Anthropic is an AI lab just like OpenAI. It uses GPUs, TPUs and Trainium chips. It trains models in much the same way to do much the same things, and builds quasi-functional plugins on top of them, just like OpenAI does. It makes big compute commitments, it had its infrastructure built out for it by hyperscalers, its CEO is annoying and beloved by cretins, and its value is largely determined by 1000 people on “X The Everything App” experiencing varying levels of AI psychosis.

Attempts to claim otherwise are tacit admissions that OpenAI is unsustainable.

The Victims and Consequences of the OpenAI Bubble

Please note that when I say “victims,” I don’t always mean “people you should feel sorry for.” In some cases I’ll be talking about real people who are facing the horrible consequences of the OpenAI bubble bursting, and for whom you should feel a degree of sympathy, and in others, I’m referring to various Patagonia gargoyles’ financial woes. I assume you’ll be able to differentiate between them.

Consumers, The Victims of A Great Memory Crisis That Sam Altman and OpenAI Helped Start

My last premium newsletter was the massive Hater’s Guide To The Memory Crisis, or the twisted tale of how three companies — Samsung, SK Hynix and Micron — have diverted meaningful amounts of manufacturing supply away from making the RAM you find in laptops and smartphones toward making the high-bandwidth memory that powers GPUs, jacking up the price of consumer electronics in the process.

To explain:

An AI data center is full of servers, which are in turn full of (for the most part) NVIDIA GPUs. Each NVIDIA GB300 has two B300 GPUs, the two of which have 576GB of High Bandwidth Memory (HBM, or HBM3e to be specific), and a CPU, which has 480GB of lower-power LPDDR5X RAM (the kind usually used in cellphones and other mobile devices). These systems tend to be sold in an NVL72 rack with 18 compute trays, bringing us to 36 GB300s, for a total of 20.7 terabytes of HBM and 17 terabytes of LPDDR5X RAM, and that’s before you get to the RAM associated with the high-speed networking gear and other associated components.

Because HBM takes up more space on a wafer — the slice of semiconductor material that is etched using photolithography (read: molten tin) and then cut into separate dies (individual chips) — and generally has much higher margins (the actual product its more expensive to make, but thanks to the triopoly of Samsung, SK Hynix and Micron, they can charge whatever they like, predominantly to NVIDIA), memory manufacturers are dedicating more space on their manufacturing lines to it than to regular consumer RAM, which allows (thanks to said triopoly) said manufacturers to charge effectively whatever they want for consumer RAM.

To simplify, the AI GPUs in AI data centers require hundreds of gigabytes of high-bandwidth memory, the CPUs attached to them require the same RAM as your smartphone, and the companies making all of this RAM are making huge profits by jacking up the price because of supply chain constraints that they themselves have created. That’s why Micron had 84.9% gross margins in the last quarter. The RAM triopoly controls more than 90% of the world’s memory, and can set prices at whatever rate they want.

These three companies were all fined over $100 million by the Department of justice back in 2002 for price-fixing, with Micron avoiding the fine by turning in its co-conspirators. Five years later in 2007, a Supreme Court judgment and resulting precedent (Bell Atlantic V. Twombly) drastically raised the bar for not simply winning an antitrust case, but even getting one to trial:

The Twombly Test/Rule was designed to raise the bar to civil legislation, so that defendants aren’t forced to comply with discovery in frivolous cases, which can be incredibly expensive.

While this seems reasonable at first glance, it makes it significantly harder to litigate any kind of antitrust action, because the market signals — whether they be pricing, or difficulties in new competitors bringing their products to market — tend to be the starting pistol on any action. The damning evidence — loose-lipped executives talking about their nefarious plans — tends to be something that shows up once the trial has progressed to the discovery stages.

This precedent would kill a 2019 class action case against SK Hynix, Samsung and Micron that alleged they had colluded to tighten the supply of the world’s DRAM, because despite statements from company representatives made at public events, their collective participation in certain industry groups, and observable pricing trends, the precedent set by Twombly meant that the plaintiffs required more than circumstantial evidence to bring something to trial.

Anyway, the reason I bring this up is that while I am not accusing Samsung, SK Hynix, and Micron of price-fixing, a recent lawsuit is accusing them of exactly that:

The suit claims the alleged anti-consumer behavior started in 2022, when the companies began shifting production from SDRAM to HBM — something that, at that point, they made “no economic sense” except as a means to hike prices.

“This plan has thus far succeeded, as consumer purchasers of conventional DRAM and devices incorporating it have paid supracompetitive prices and have otherwise suffered the impacts of a distorted market crippled by the behavior of DRAM oligopolists,” the filing states.

So, what does this have to do with OpenAI?

Well, back on October 1, 2025, OpenAI, Samsung and SK Hynix announced a “strategic partnership” that would involve OpenAI buying 900,000 wafers of DRAM a month (around 40% of the world’s supply at the time) for Stargate data centers — something that never actually happened (it was a memorandum of understanding, and OpenAI also had nowhere to put them), but both SK Hynix and Samsung’s stocks immediately rallied, and Samsung happened to hike prices by 60% a month later, which could be a coincidence, or could have been the company saying “yeah, wow, we’re gonna run out of RAM I guess, better buy now at whatever price we have it!”

Another clue that this might not all have been above board was that Samsung was reportedly doing another deal with OpenAI in March 2026, “...to supply up to 800 million gigabits (Gb) of 12-layer HBM4 chips to OpenAI in the second half of this year” per Reuters, for use with Broadcom’s custom “Jalapeno” chip. Though it’s hard to calculate exactly how much that would be wafer-wise, from what I understand we’re talking in terms of less than 100,000 wafers total after OpenAI, Samsung, and SK Hynix said they’d be taking up 900,000 a month.

Regardless of whether OpenAI ever takes a single wafer of silicon, these deals existed to put the squeeze on any company that uses memory in their products — including NVIDIA, AMD and Broadcom — which in turn led to the most aggressive price increases in the history of consumer electronics. As I said last Friday:

The net result is pretty simple: every single consumer electronic of any kind is getting more expensive. Valve’s Steam Machine console debuted at a 30% higher price point than planned, Apple hiked the prices of its MacBooks and iPads and will likely have to do the same for its next iPhone. Nintendo, Microsoft and Sony increased the cost of their consoles, and the PS5 and Xbox Series now cost more today than they did when they first retailed, almost six years ago.

And yes, OpenAI is responsible, both in its naked collusion with memory manufacturers to push an announcement that never resulted in anything other than price increases and its siren song that made every dimwit with debt desperate to build AI data centers.

Every single consumer suffers as a result. RAM is in everything, and it’s unclear when new manufacturing capacity will actually come online, as fabs are expensive and complex construction efforts and require tons of specialist talent, raw materials, permitting, land and power. SK Hynix Chairman Chey Tae-won said in March that the memory shortage would last until 2030, and he may be right, as a Bank of America report just said that SK Hynix may only be able to add a sixth of its planned capacity by 2028.

This means that the price of consumer electronics will be inflated for the foreseeable future, even if the AI bubble bursts. While capex pullbacks will eventually happen and by extension eventually lead to supply constraints easing, Micron, Samsung, and SK Hynix had sold out their entire 2026 supply by the second week of January, and noted that they’d only be able to handle 60% of “medium-term” customer memory orders, which suggests to me that 2027 might be even worse, with a subtle clue being that SK Hynix CEO Kwak Noh-jung recently told Reuters that 2027 would be “the worst year in the industry’s history from a supply perspective.”

While the memory triopoly has every incentive to make things seem bleak to drum up business and sustain their margins, behind the scenes reports suggest they’re turning the screws on everybody.

Speaking with Steve Burke of GamersNexus for my podcast Better Offline (out next week!), I learned that consumer electronics companies have told him in private that they’ve never seen anything like this — and that the average purchasing experience for buying RAM now involves being told a price that you either accept or never get to do business with the RAM companies again.

This is a graphic example of companies with massive amounts of leverage using it to fuck over both their customers and their customers’ customers.

Who gave them that leverage? The AI industry and Sam fucking Altman.

Retail Investors, And How OpenAI and Sam Altman Helped Enshittify The Stock Market With The AI Trade

Hey, remember when I just said that (it seems, but I cannot confirm that) OpenAI helped SK Hynix and Samsung manufacture a supply chain crisis last year using a phoney announcement for a project that would never happen?

That happened three other fucking times in the same three week period, and modern journalism doesn’t seem to give much of a shit!

Let’s review what happened, per my year-ending Enshittifinancial Crisis newsletter:

- On September 22, 2025, NVIDIA announced a “strategic partnership” to invest “up to $100 billion” and build 10GW of data centers with OpenAI, with the first gigawatt to be deployed in the second half of 2026. Where would the data centers go? How would OpenAI afford to build them? How would OpenAI build a gigawatt in less than a year? Don’t ask questions, pig!

- NVIDIA’s stock bumped from from $175.30 to $181 in the space of a day. The media wrote about the story as if the deal was done, with CNBC claiming that “the initial $10 billion tranche [was] expected to close within a month or so once the transaction has been finalized.” I read at least ten stories that said that “NVIDIA had invested $100 billion.”

- This deal never happened. Three months later, the Wall Street Journal said that it was “on ice,” and two months after that, NVIDIA pledged to invest $30 billion in the company, and though NVIDIA mentioned investing $18.6 billion in “private companies and infrastructure funds…[including] AI model makers that may indirectly purchase or use our products in the cloud,” it’s unclear how much made it to OpenAI.

- On October 5, 2025, AMD announced that it had entered a “multi-year, multi-generation agreement” with OpenAI to build 6 GW of data centers, with “the first 1GW deployment set to begin in the second half of 2026,” calling the agreement “definitive” with terms that allowed OpenAI to buy up to 10% of AMD’s stock, vesting over “specific milestones” that started with the first gigawatt of data center development. Said data centers would also use AMD’s yet-to-be-released MI450 GPUs. The deal would, per Reuters, bring in “tens of billions of dollars of revenue.”

- AMD’s shares surged by 34%, with analyst Dan Ives of Wedbush saying that this was a “major valuation moment” for AMD.

- I can find no tangible evidence that OpenAI has bought a single AMD GPU. While its most-recent 10K references a “product purchase agreement with OpenAI OpCo LLC,” and while you can sort of blame the rumoured delays of the MI450 GPUs OpenAI is supposedly buying, it’s weird that AMD hasn’t loudly mentioned this on every earnings call. It’s also weird that in February 2026, Meta and AMD signed a near-identical agreement.

- On October 13, 2025, Broadcom announced a 10 gigawatt deal with OpenAI, claiming that it would deploy 10GW of OpenAI-designed chips, with the first racks to deploy the second half of 2026 and the entire deployment completed by end of 2029. Broadcom's stock popped by 9% on the news about the 10GW deal, with CNBC adding that "the companies have been working together for 18 months. [emphasis mine, for a reason that will soon become obvious]"

- On May 7, 2026, The Information reported that Broadcom and OpenAI had yet to work out how to finance the initial purchase of its specialist chips. On June 24 2026, OpenAI and Broadcom would announce the chip had been “developed from design to production in nine months,” the kind of blatant lie that you tell when you know nobody in the media is watching.

- On December 11, 2025, The Walt Disney Company announced that it had reached a “landmark agreement” with OpenAI to bring its characters to Sora, adding that it would invest $1 billion in the company. The same day, Disney CEO Bob Iger and Sam Altman went on CNBC, with Iger adding that Disney “[wanted] to participate in what Sam is creating, what his team is creating,” and added that Disney “thought this is a good investment for the company.” It would also buy ChatGPT for the entire company.

- On March 24, 2026, OpenAI announced Sora was dead, the deal was dead, and it’s unclear whether anything actually happened.

All four of these companies’ stocks rallied on deals that land somewhere between misleading and fictional, with basically anyone who invested in them being underwater within two months, though all three have recovered thanks to similarly-questionable announcements and deals made by companies with the sole intention of boosting their stocks.

Sidenote: I didn’t even bring up what happened with the entirely-fictional $500 billion “Stargate” Project with Oracle and OpenAI, because I’d write another 200,000 words about how everyone who helped pump it should feel ashamed of themselves.

The same goes for every single analyst who reacted to Oracle’s OpenAI-driven remaining performance obligations like a horny teenager seeing his first boob. The capacity never existed, this deal will never happen, and you all know it and are either hopelessly ignorant or craven beyond words.

Why else would Sam Altman go on CNBC with NVIDIA CEO Jensen Huang on the day of an announcement of a project that was only ever a letter of understanding? Why else would Sam Altman jump on TV with Bob Iger to talk about a Disney deal that clearly never went anywhere?

Spare me any explanations around the “fast-paced dealmaking of AI” or “how deals are complex.” CNBC reported the day after the NVIDIA deal was announced that the first $10 billion tranche would “close within a month or once the transaction had finalized” via a source! It’s blatantly obvious that the intention was to create the appearance that a deal existed that never actually existed at all!

The AI trade is the natural endpoint of an increasingly-enshittified stock market where many analysts and journalists exist only to repeat narratives to influence stock prices. Outside of semiconductors, the AI trade has never, ever been about the actual underlying economics or the actual economic potential of Large Language Models, but projecting shadows on the wall to resemble something that looks like the next generation of technology.

That’s because the AI trade is entirely symbolic and driven by stock prices. When NVIDIA and the rest of the Magnificent Seven (sans Apple) does well, AI is the greatest thing on Earth. When the Magnificent Seven stumbles, everybody worries that they might be overspending on AI. The AI trade exists only to manipulate stock prices through spurious news and smoke signals on social media, and to drag gullible retail investors (who account for 20% of US equity trading volumes, the highest it’s been since 2021) and the rest of the market away from caring about things like “fundamentals” or “reality” toward whatever keys are currently jingling.

My evidence is fairly simple: Google, Meta, Microsoft, and Amazon don’t actually tell you their AI revenues, other than when Microsoft and Amazon have chosen to define it in terms of undefined “run rates.” And why would they? Reporters have been saying that their AI bets have paid off for years without the companies ever having to show it paying off other than their stocks running.

Here’s another example: CoreWeave, a time bomb/AI compute company that only really exists as a revenue source for NVIDIA (per Jensen Huang, if [NVIDIA] didn’t help CoreWeave exist, they would not exist”) by signing contracts with companies for unbuilt capacity that it then takes to banks and uses to raise more money to buy GPUs. NVIDIA knows that analysts and reporters don’t give a shit about the blatant self-dealing and circular financing, all because these deals help the stock price go up, which apparently is the only metric that modern journalism evaluates. That’s why when NVIDIA invested $2 billion in CoreWeave in January 2026 — a warning sign that the company had liquidity problems! — led to endless positive coverage after “the stock popped on the news,” per CNBC.

That’s because the AI trade exists only to extract value and con investors. It is not a trade related to the actual fundamentals of whether AI works or not, whether AI actually makes anyone money, or really anything about AI at all outside of whether mentioning AI or an AI-related company makes a stock number go up or down.

I’ll be blunt: modern journalism has failed the retail investor and directly helped the wallet inspector regulate the stock market. By empowering Sam Altman and the rest of the AI industry’s deliberate attempts to obfuscate the actual economics of generative AI and setting the terms of AI’s success as “how stocks are doing and whether the companies are growing in general,” they have defaulted on their responsibility to the general public and helped the already-rich get richer.

None of this would be possible if business journalism actually saw themselves as having a responsibility to give their audience good information. While one could argue that if you had blindly invested in the AI trade you might have made money, the ability to make money in the AI trade was directly driven by modern journalism’s inability or unwillingness to push back on any corporate narrative. Every major outlet ran a story on every one of the deals I mentioned, and not a single one seemed remotely upset or deterred by the fact they were misled, and in turn misled their audience.

And yes, investment funds can be just as easily manipulated as a retail investor, and will follow whatever trend seems likely to make them money, even if said trend is utterly disconnected from any fundamentals. Tech analysts help do so by creating vast models that give a veneer of respectability, even if their projections mostly amount to “number will always go up in the future.”

This is why Musk was able to dump SpaceX on the public markets. Why SK Hynix chose to list on the NASDAQ. When the entire world is captured by a childlike belief that “AI is good and will be the biggest thing ever,” you empower grifting and swindling at scale.

Well, that and underwriters like Goldman Sachs are so nakedly crooked that they’ll say they expect SpaceX’s AI revenue to grow 100x by 2030. Fuck off!

Yet the memory boom/bust/crisis is where the media has failed investors the most — a final insult before everything collapses.

You see (to quote myself), what makes this particular memory crisis so distinctly dangerous is that it isn’t a result of consumer demand so much as it is capital expenditures from very large companies making bets that don’t connect with reality.

Microsoft, Google, Amazon, and Meta aren’t spending $765 billion in capex in 2026 because of rapid demand by consumers for AI services, but a desperation caused by a lack of hypergrowth ideas, circular financing with Anthropic and OpenAI, and a vague concern that if they stop spending that the other guy will do something as a result.

Anyone blathering on about a “memory supercycle” is intentionally obfuscating where that revenue and demand is coming from — high-bandwidth memory attached to AI GPUs, meaning that this boom cycle only exists as a symptom of a greater hype cycle, meaning that when companies stop buying GPUs, the demand for that (briefly) high-margin high-bandwidth memory goes with it.

To give you some context, a chart from ComputerBase.de showed that high-bandwidth memory demand grew from 681 million gigabits of HBM in 2022 to 29.3 billion gigabits on 2026 — a 40x increase over the course of four years that suggests that once GPU-related capital expenditures stop, high-bandwidth memory demand will effectively disappear.

As I mentioned previously, this isn’t even me being a hater. Hyperscalers are now joining the rest of the world in having to raise debt to buy more GPUs, which means that at some point they aren’t going to be able to afford to buy as much, which will in turn mean that NVIDIA — which accounts for around 65% of all HBM purchasing — won’t need as much.

I have not read a single fucking article that mentions that this is a possibility! Every article about the memory industry right now is about supply constraints and the increasing cost of memory, but none of them warn investors or the general public about what will happen when capex slows, and certainly not the many, many articles in major business publications about SK Hynix, Samsung and Micron’s revenues. In fact, Reuters said that SK Hynix’s “scarcity premium looks built to last.”

The cynical (and boring) response here is that “the market can stay irrational longer than you can stay solvent,” but saying that distracts from the larger point of how said irrationality was manufactured by the media.

Sidenote: There’s plenty of evidence that AI has a pathetic effect on revenues. For example, it took Salesforce three years to get to $1 billion in AI ARR (read: $83 million a month for a company with revenues of $40 billion+ a year), a pathetic amount that should have had people running for the hills…except journalists were saying its AI bet had “paid off” months beforehand. It would be easy — and responsible! — to call this out.

I am not sure what the majority of the media sees as its purpose or responsibility to its readers, so I will speak plainly: the responsibility is to tell them the cold, hard truth, rather than going along with whatever hype cycle is happening out of fear of being wrong or missing out. Skepticism is not doomerism! Being critical is not being negative! These companies are some of the largest and richest enterprises in the world — they should be scrutinized!

And no, scrutiny is not publishing everything they say and then making a vague comment about “whether or not that bet will pay off.” Too often, journalism conflates objectivity with passivity, seeing critiques as “negative” or “biased” when, in fact, repeating everything that corporations say to their benefits is about as biased as it gets.

In the end, the victims are anybody who doesn’t exit the AI trade in time.

Sidenote: It seems increasingly likely that “anybody” will be retail investors, with Citadel Securities noting earlier this week that “retail remains the strongest structural buyer of US equities,” and that it hasn’t seen a single day in the month of July where retail investors were net sellers of stocks, rather than buyers.

Things are similarly bleak in South Korea — where retail investors aren’t just some of the biggest buyers of equities, but they’re doing so on margin.

By the way, there’s no Hell hot enough, by the way, for the people that will read this and smugly say “heh, well, I made money,” or who point to anyone’s returns as evidence that the AI trade is anything other than manufactured consent. The fact that anyone made money on this trade is a sign that the stock market is inherently manipulated to benefit the wealthy at the cost of the many — and when the bubble bursts, the people that will suffer will have suffered because of the media’s participation by helping Sam Altman and the rest of the AI industry obfuscate and twist reality to pump stocks.

Which leads us neatly to our next victim!

SoftBank, Masayoshi Son, and Japanese Retail Investors

In my Hater’s Guide To SoftBank, I told the story of CEO Masayoshi Son, a degenerate gambler who has steered his company through boom and bust cycles only through the grace of whatever God he believes in and sheer luck.

SoftBank Group — the holding company, and not to be confused with Softbank Corp, which runs a bunch of telcos and media companies in Japan — makes money only through either investing in or buying companies, then taking them public or selling them to someone else, and otherwise needs debt for liquidity.

Masayoshi Son makes terrible bet after terrible bet, but his luck always seems to work out for him. His $20 million stake in Alibaba turned into $50 billion at IPO. He bought a 70% stake in Sprint that turned into a 24% holding in T-Mobile. In the early 2000s, Softbank took a 23% stake in Betfair that eventually became part of the $17.7 billion Flutter Entertainment. And then there’s its most-recent and arguably most-impressive (after Alibaba at least) investment, ARM, which it acquired for $32 billion in 2016 and then took it public in 2023 at a valuation of $54.5 billion, and currently sits at around a $300 billion market cap.

Sidenote: SoftBank Group is “valued” based on the “net asset value” of its holdings (which you can see here), and whenever you’ve seen it have “losses,” that’s because the underlying value of its assets (many of which are privately-held companies as part of its disastrous Vision Funds 1 and 2) is what gives it is “returns.”

This is why SoftBank was able to book a yearly gain of $46 billion for its Vision Fund 2 thanks to its investments in OpenAI, despite losses from DiDi Global, Coupang, and Klarna.

Yet his problem has always been his dalliances with whimsical white boys. SoftBank sunk $1.5 billion into dodgy financial services firm Greensill Capital before its collapse, and in the aftermath, it was revealed that Masayoshi Son and CEO Lex Greensill talked on the phone every day, to the point that (per Greensill himself) SoftBank managers felt “threatened” by Greensill’s relationship with Son. It only took Masayoshi Son 28 minutes of conversation with WeWork’s Adam Neumann before he drew up the terms for a $4.4 billion investment on his iPad and signing the deal in the back of a cab, with Son saying that “the last person he felt this with was [Alibaba CEO] Jack Ma.”

And no white boy has ever been more whimsical than Sam Altman.

In 2019, Altman turned down $10 billion from Masayoshi Son (which, ironically, would’ve been an incredible investment at the time), going instead with $1 billion (and full infrastructure support) from Microsoft, and I believe this moment drove Son into a level of madness that will potentially wreck the company.

You see, up until fairly recently, SoftBank had been dragged down by the declining value of its atrocious investments via its two venture capital funds — Vision Fund 1 and 2, the latter of which was self-funded and has mostly gone toward funding OpenAI. Up until recently, SoftBank had quarter after quarter of losses as investment after investment saw its NAV drop because, well, they were overvalued and SoftBank never should’ve invested in them in the first place.

To survive, SoftBank moved into “defense mode” in 2020, slowing investments and selling the vast majority of its Alibaba stock by April 2023, with the ARM IPO and billions of dollars of bond sales helping slow the bleed.

Yet Masayoshi Son knew he was destined for greater things, as he told CNBC in June 2024:

“SoftBank was founded for what purpose? For what purpose was Masa Son born? It may sound strange, but I think I was born to realize ASI. I am super serious about it,” Son said.

OpenAI — and the larger AI trade — had given Masayoshi Son a certain kind of greed-driven mania, where he believed that AI would make SoftBank (as he said recently) “the goose that laid golden eggs,” an eternal money-printer that ostensibly started with the biggest cash-burning machine in history.

Altman, like Neumann, like Greensill, told Masayoshi Son exactly what he wanted to hear: that this would be the biggest thing ever, and that Son would capture all of the value both through his investment in OpenAI and further investments in data centers and other AI infrastructure.

And so began his most vulgar investment yet — OpenAI, sinking $2 billion into the company from Vision Fund 2 in November 2024 — only for Altman to turn around and demand he fund $30 billion of a $40 billion round that would get announced four months later in March 2025.

Masayoshi Son was an emphatic “yes,” except for one little problem: he didn’t have the money, and could only afford the first $7.5 billion (due in April 2025) by taking out a $15 billion, year-long bridge loan, with the rest of it going toward his eventual purchase of Ampere computing.

To fund the remaining $22.5 billion, SoftBank was forced to take out further margin loans on its ARM stock, and sell large chunks of its T-Mobile stock, as well as its entire $5.83 billion stake in NVIDIA.

Yet as soon as the check cleared, Sam Altman was blowing up his phone demanding more money as part of a $110 billion funding round in February 2026 (that eventually became $122 billion in late March).

Masayoshi Son was once again an emphatic yes, except by this point he’d exhausted basically every useful thing left in his coffers outside of around $118 billion in ARM shares that make up around 40% of SoftBank’s net asset value, meaning that selling or using further ARM shares as collateral would directly tank its value — both through the obvious “they have less of a valuable thing” and sales/collateralization of further ARM shares affecting its share price.

So, what did Masayoshi Son do? More debt, baby! More risky debt! You can always refinance it, right?

To pay for its share of OpenAI’s 2026 funding round, SoftBank took out a $40 billion bridge loan (maturing in March 2027), bringing its investment in the company to over $40 billion, with its payments to $10 billion tranches of OpenAI funding due in April, July and October 2026.

A few months later, it tried to raise a $10 billion margin loan using its entire OpenAI investment as collateral, cut the amount it was raising to $6 billion, and when banks remained hesitant to give it the money anyway offered to “guarantee repayment of the loan to address lender concerns,” effectively backing the loan with its own balance sheet (called a recourse loan) because, despite being worth over $100 billion on paper, its lenders had doubts that its OpenAI stake was actually worth that much.

If you’re wondering why it didn’t simply take out more debt, it’s because (as a result of its continuing investments in OpenAI) S&P Global revised SoftBank’s outlook to negative, emphasis theirs:

The liquidity of SoftBank Group's investment portfolio will worsen because OpenAI now accounts for a bigger share of it. OpenAI Group PBC is a privately held U.S.-based AI research and development startup company. SoftBank Group's additional investment amount will be $30 billion (about ¥4.5 trillion).

The creditworthiness of the company's investment assets will also likely deteriorate. We see OpenAI as one of its investments with the weakest credit quality. The company's investments in AI, including OpenAI, mostly involve fledgling startups and private companies that we believe are exposed to significant AI innovation risk and fierce competition.

This has had a knock-on effect on the rating of the telecoms-focused Softbank Corp (as a reminder, Softbank Group is the holding company that owns stock in other companies, Softbank Corp is the energy/telecoms company that actually makes stuff), which is now rated BBB, or the lowest-possible rung of investment-grade financing in the S&P system.

To make matters worse, if SoftBank continues to hold a loan-to-value ratio of above 30% for much longer, it runs the risk of its debt getting downgraded even further, which would slam the door shut on its ability to raise money via bonds, which is…well, basically how SoftBank has functioned for the last 10 or 20 years.

And this is all happening as Japan is determinedly inching away from the era of persistently low interest rates — making debt far more expensive to service.

SoftBank needs OpenAI to IPO so that it can turn that on-paper gain into actual liquid stocks that can be dumped into the market or used for real-life margin loans. SoftBank has jettisoned the vast majority of its heaviest-weight investments, leaving it largely dependent on the continued value of ARM’s stock to keep its seat at the table, and if OpenAI can’t go public, it’ll end up sitting on illiquid stock in a company that will see its value tank as a result.

Yet even if OpenAI does go public, any attempts to get a margin loan will likely be dangerous, as I bet that it will be one of the single-most shorted and volatile stocks in history, which will also be a problem for SoftBank’s underlying net-asset value, which will ebb and flow based on whatever bullshit Altman cooks up every three months.

Masayoshi Son is both a victim of the manufactured consent of the AI trade and an enabler of its worst excesses, empowering and enriching Sam Altman at a time when any kind of financial prudence might have curbed OpenAI’s greed or killed it before it caused further damage.

SoftBank tanking will fuck over anyone invested in the Japanese stock market, where it currently sits as the third-largest company by market cap behind KIOXIA (a memory company booming thanks to the AI trade) and Mitsubishi UFJ Financial (a bank with heavy ties to the AI industry and data center infrastructure). While I severely doubt it’ll die — it’s likely MUFJ and SMBC Bank would extend whatever credit necessary to keep the doors open — OpenAI and the greater AI trade has become a load-bearing toothpick holding up the trillion-ton ass of the world’s most well-funded gambler.

For SoftBank to survive in its current form, OpenAI must go public, become a thriving and profitable business, and have its stock price stay elevated for the foreseeable future. Additionally, ARM must also retain or exceed its current stock price.

Hey, while we’re on the subject of “companies betting the entire future on OpenAI that recently got downgraded by S&P Global…”

Oracle, And Larry Ellison’s Fortune

Hey! You in the back! Stop laughing! Stop laughing at Larry Ellison! He’s now only the world’s 8th-most-richest guy!

Just kidding, fuck Larry Ellison. What I’m about to tell you might make you laugh, probably because it’s really funny.

Oracle is currently spending over $340 billion to build out over 7.1GW of data center capacity for OpenAI, as part of its $300 billion, five-year-long cloud compute contract that began, at least in theory, on June 1, 2026 at the beginning of its Fiscal Year 2027, though much of the capacity is yet to be built. To fund the buildout, Oracle has had to raise over $50 billion via stock sales and debt, spent $55.7 billion in its last fiscal year, and expects to spend at least $90 billion more in FY2027.

As a result of that, S&P Global downgraded Oracle’s credit rating to BBB/A-2, the literal lowest level before it’ll become junk-grade, meaning that one more downgrade (though it would have to be from two ratings agencies) from here would risk Oracle becoming a “fallen angel,” with investment funds (that can’t hold junk grade debt) having to jettison its debt from indexes, as happened to Ford in March 2020, leading to over $35 billion in debt being dumped and its borrowing costs skyrocketing to between 8.5% and 9.625% when it raised in April 2020. For some context, Ford reported an average interest rate of 5.2% on its long term debt in its 2019 annual report.

You’ll never guess why S&P Global downgraded Oracle! And, once again, the emphasis is theirs:

OpenAI remains a key credit risk. We estimate that OpenAI makes up roughly half of the $638 billion in RPO. OpenAI’s ability to meet its contractual obligations and raise external financing will be contingent upon AI tailwinds continuing and its models being market leaders. If OpenAI were unable to pay Oracle, we believe Oracle could be left with massive data center leases that it might be unable to exit or have to re-lease to new tenants under less-favorable terms. As a proxy for OpenAI’s future prospects, we’re tracking OpenAI’s financial commitments to data center operators and chip makers to gauge its overall financial exposure and its market share among enterprise and consumers.

That’s a load-bearing if, brother!

Anyway, you know who else is trying to warn you about Oracle’s exposure to OpenAI?

Oracle! Per Bloomberg:

Oracle has a new warning for investors: All of the spending on data centers might not pay off.

The disclosures were part of the company’s annual financial report, where Oracle detailed plans to spend big on AI infrastructure for customers like OpenAI. And it noted all of the ways that expensive bet could blow up. Construction of data centers may end up costing more or taking longer than expected, Oracle warned. This could happen due to supply chain hiccups, government restrictions on data center development, or the failure of third parties to complete projects on schedule.

And once the sites are done, major customers might not pay their bills, or opt not to renew their contracts, Oracle said. In this case, the company could be stuck with some very expensive assets, which it “may be unable to re-lease, repurpose or assign such capacity on acceptable terms, if at all.”

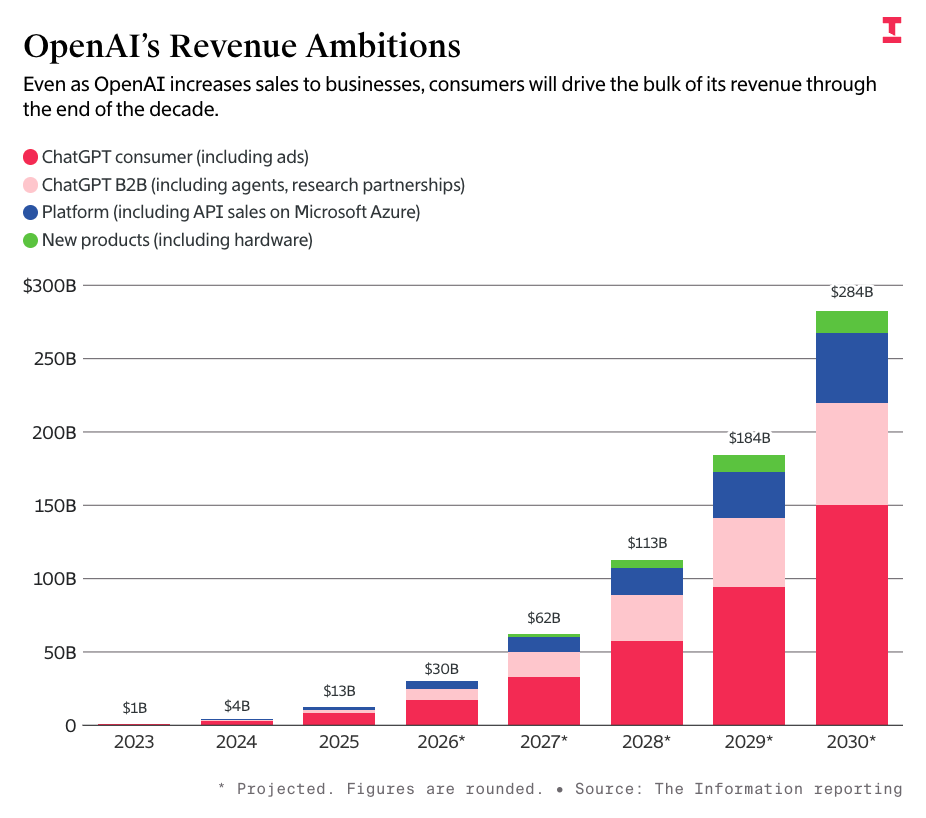

As a reminder, the only way that OpenAI will be able to afford to pay its $300 billion cloud compute contract with Oracle will be if it continues to hit revenue projections (per The Information) that have it making $113 billion in 2028, $184 billion in 2029, and $284 billion in 2030, a year when it will magically become profitable, and no, I don’t know how that happens:

Based on my own analysis, assuming that Oracle can successfully build capacity for OpenAI to pay for (a load-bearing assumption), it would have to pay around $75 billion to rent that 7.1GW of capacity. Stargate Abilene, an 8-building, 1.2GW project that broke ground in July 2024, has (per sources familiar with the matter) only built and operationalized three buildings, despite the project having meant to be fully operational by the end of 2025 (per landowner Lancium), or energized by the middle of 2026, it isn’t really clear, and I can’t get a straight answer from anyone about whether the power even exists on site to turn any of it on.

Anyway, for Oracle to make all the rest of that money, it will have to build five more Stargate Abilenes. If you’re wondering how that’s going, Stargate Shackelford only broke ground in December 2025, Stargate Wisconsin appeared to have a single steam beam in March, Stargate Michigan only got its first steel beams two months ago, and Stargate New Mexico is still waiting for permitting to begin construction.

Based on Lancium’s presentation and discussions with sources familiar, Oracle will pull in somewhere in the region of $10 billion in annual revenue from the (assuming it’s ever done), completely-finished 824MW of critical IT infrastructure at Stargate Abilene. It is unclear how Oracle hopes to be paid even a fraction of its $300 billion compute deal, because in its current state, its annual revenue from Stargate projects currently sits in the region of a maximum $5 billion a year, or less than a tenth of its FY2026 capex.

For the most part, Oracle has funded the various Stargate data centers with project financing, meaning that a nebulous SPV will be responsible in the event it defaults on any of these contracts…until Stargate Michigan, which only closed when Oracle agreed to guarantee the $14 billion in bonds raised.

All of this revenue — both theoretical and otherwise — sits in Oracle’s “Cloud” segment, the only part of the business that’s actually growing, as the rest of its business has either been declining or plateauing for about a decade.

In any case, for Oracle to actually get paid its $300 billion, it will have to build upwards of 6GW of data center capacity…in a year and a half? This deal is meant to be worth in the higher range of tens of billions of dollars in annual revenue by FY2028, which begins on June 1 2027! Stargate is horribly, impossibly delayed, to a level that makes me wonder if anybody other than perhaps Anissa Gardizy has bothered to think about Stargate for even a fucking second.

Anyway, Oracle’s entire future rides on this deal. While Oracle Cloud Infrastructure continues to grow, its future growth (and remaining performance obligations) almost entirely hinge on both its ability to build the largest infrastructure project of all time and for OpenAI to continue raising funding for an indefinite amount of time. The rest of that growth comes from Meta and xAI, both of whom are only really “doing AI” because everybody else is.

This puts Oracle in a very, very compromising position on multiple different levels.

Generative AI is the only reason that Wall Street started liking Oracle again as its other business plateaued, even as it burned billions of dollars on capital expenditures and cut its gross margins by a little under 15% since 2022, with the vast majority of that value coming from its revenue from OpenAI and what’s actually active at Stargate Abilene.

Much like the rest of the AI trade, everything about Oracle’s future is sold on potential rather than anybody thinking about reality or things like “whether Oracle can actually build the data centers” or “how Oracle makes any of that revenue if the data centers aren’t built” or “how OpenAI affords to pay for the compute if the data centers get built.”

As Oracle said in its own disclosures, if OpenAI can’t pay, “Oracle could be left with massive data center leases that it might be unable to exit or have to re-lease to new tenants under less-favorable terms,” and there isn’t a single company on Earth who can or would pay for such a large amount of compute, nor is there the aggregate demand to justify it.

Sidenote: No, Anthropic can’t afford it either, and Sundar Pichai would unhinge his jaw and swallow Oracle whole rather than see it move off of its TPU infrastructure.

While its many government contracts and national security significance make it unlikely that Oracle would be allowed to die, the collapse of its only growth segment will likely spell dark times for a company that’s already laid off 21,000 people as a means of funding its AI buildout.

The double-edged sword of the AI trade’s childlike attachment to stock valuations poses an egregious threat to Larry Ellison himself.

How OpenAI Might Destroy The Ellison Fortune

Hey — HEY! I said no laughing! Stop it!

This is all very serious! This is a serious situation! You’re laughing about the potential downfall of a guy who once wrote a letter to the New York Times attacking HP for firing former CEO Mark Hurd for repeatedly making sexual advances toward a reality star using HP’s finances!

Sorry, my mistake, you should keep laughing, even the prospect of what I’m about to tell you is hilarious.

As I said in my piece about how OpenAI Kills Oracle:

[The collapse of Stargate and OpenAI would be] a very bad thing for Larry Ellison, who holds around 40% of Oracle’s shares and receives a dividend of around $2.3 billion a year as a result, especially as he’s backed the $111 billion Paramount-Warner Brothers Discovery merger deal with $45.7 billion of that as an equity commitment from the Ellison Trust (the Ellison family investment arm which holds his Oracle shares) with Larry himself guaranteeing the amount, with $24 billion of those funds likely coming from the Middle East.

This leaves the Ellison family with around $12 billion left to fund the deal. Depending on how liquid the trust is, it could foreseeably fund that in cash, but if Ellison is a little light, he might have to take out further margin loans on his Oracle stock.

Yes, I used the word “further.” Ellison has already pledged 346 million shares of his Oracle stock — or around $61.5 billion — “to secure certain personal indebtedness, including various lines of credit,” meaning “many big, beautiful loans against his Oracle shares.” which IFR estimated back in September (when Oracle’s stock price was much higher) could allow him to secure as much as $21.4 billion in debt at a (they say “conservative”) loan-to-value ratio of 20%, and that’s assuming the banks weren’t particularly generous.

One of the consistent themes of this piece is that much of the “value” of AI is hot air — by which I mean whatever people are willing to pay for a stock that’s continually inflated by specious media-driven hype.

Ellison’s wealth is driven by both his share of Oracle’s ongoing yearly dividend, his Oracle shares, and his ability to offer said shares as margin loans, which makes him vulnerable to even a symbolic collapse of OpenAI, which is why it had to tweet in February that “the NVIDIA-OpenAI deal has zero impact on its financial relationship with OpenAI” to calm those dumping the stock.

To be clear, Ellison has around 1.16 billion Oracle shares, leaving him with around 810 million or so left, allowing him to pledge them as further collateral rather than having to either dump them on the market or dip into his reserves of about $10 billion in cash and $15 billion in Tesla stock, with Ellison historically never selling more than about $4.7 billion in stock.