Soundtrack: Ozzy Osbourne — Mr. Crowley

A lot of people have been making a lot of fun of the SoftBank 46th annual shareholder meeting and Masayoshi Son’s (to quote Bryce Elder of the Financial Times) Untethered Goose Game, specifically referring to slides that, well, looked like this:

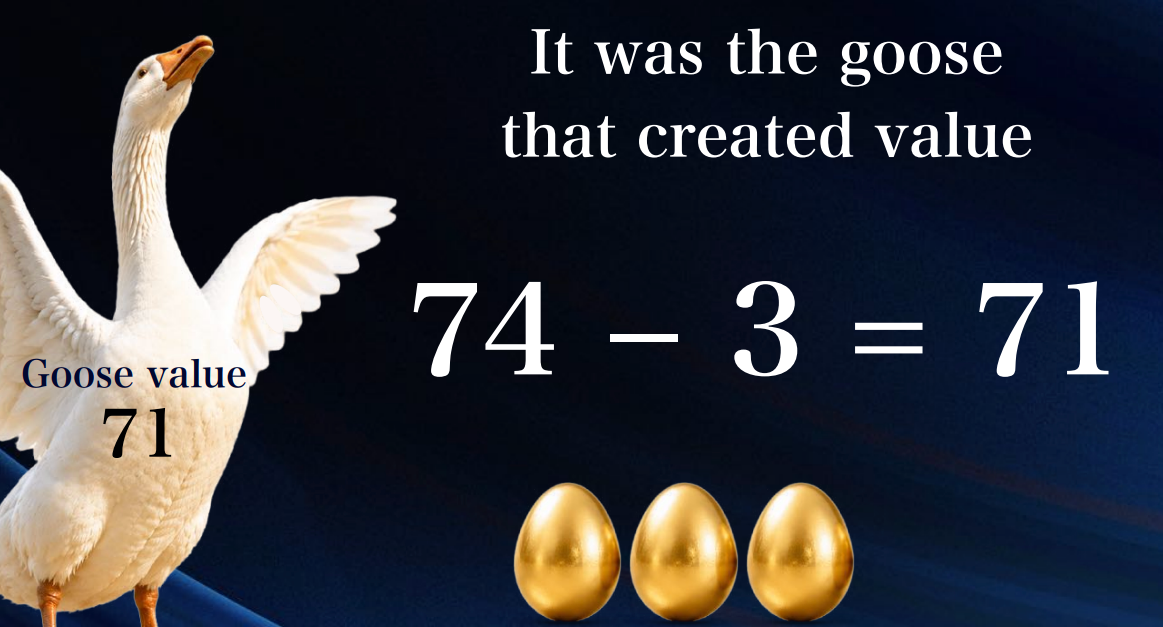

As funny and silly as these slides might be, they’re actually very indicative of the mindset behind SoftBank. Each one of those golden eggs refers to a trillion yen (about $6.15 billion) in the Net Asset Value (NAV) of SoftBank’s holdings, with the minus referring to its debt.

It’s actually very simple, especially if you know anything about geese.

Sidenote: also, before we go on any further, I need to be clear that there are two SoftBanks.

The first is SoftBank Corporation, which has a bunch of consumer businesses, all mostly in the Japanese market. It owns the Softbank-branded mobile provider, sells fixed-line broadband connections, and owns a big chunk of the company that operates the (still wildly relevant) Yahoo! Japan. It also dabbles in household utilities and electronics retail.

The second is the parent company of the Softbank Corporation, which is (confusingly) called the SoftBank Group. This is largely a holding company, and directly operates the various Vision Funds you’ve heard about. the holding company.

That’s not to say there isn’t any overlap. On Thursday, July 2, Softbank announced the launch of Softbank Neo — a US-based neocloud that plans to leverage the group’s “10-gigawatt-scale energy and AI infrastructure currently under development.” That’s a very load-bearing “under development.”

Anyway, Softbank Neo will be 51% owned by Softbank Corp (which, incidentally, has an investment-grade credit rating, whereas its parent does not), and Softbank Group will own the remaining 49%. Because this isn’t confusing enough, Softbank Neo will be, at least organizationally, treated as a subsidiary of Softbank Corp.

Regardless, or the sake of this newsletter, whenever I say “SoftBank,” you should assume that I’m talking about SoftBank Group, unless stated otherwise.

SoftBank is the goose. Masayoshi Son is the gander. Masayoshi Son mounts and impregnates SoftBank — by which I mean invests money in companies using SoftBank’s funds — at which point the goose (SoftBank) becomes pregnant (the portfolio company grows larger) and then lays the egg (the portfolio company goes public). Basically, SoftBank is a company that invests in companies that then go public and make SoftBank money, at least in theory.

To continue mounting the geese, SoftBank takes on a constant flow of debt either by raising it via the bond market, taking margin loans out using its shares in successful investments like ARM or Alibaba as collateral, or (in times of trouble) outright selling shares in companies like T-Mobile or NVIDIA.

Softbank has around $50.5 billion worth of outstanding notes as of writing this sentence, not including other forms of debt, like commercial paper and traditional loans. Including those brings the total to an astonishing $76.431 billion. And, again, this is just the Softbank Group – and not any of the other affiliated entities, who have their own balance sheets and separate reporting.

Sidenote: One thing to note is that describing Softbank’s debt is tricky, insofar as it’s a massive conglomerate with a bunch of different, nominally-independent entities, all of which can raise debt on their own merit (and, in the case of Softbank Corp, have better credit ratings than its parent, the Softbank Group). If we include the debt owed by the various other parts of the business, we end up with a figure that’s much, much bigger than $50.5 billion.

The goose-to-egg process begins to fall apart when SoftBank is unable to convert its investments into a liquid asset or margin loan, as I’ll get to later.

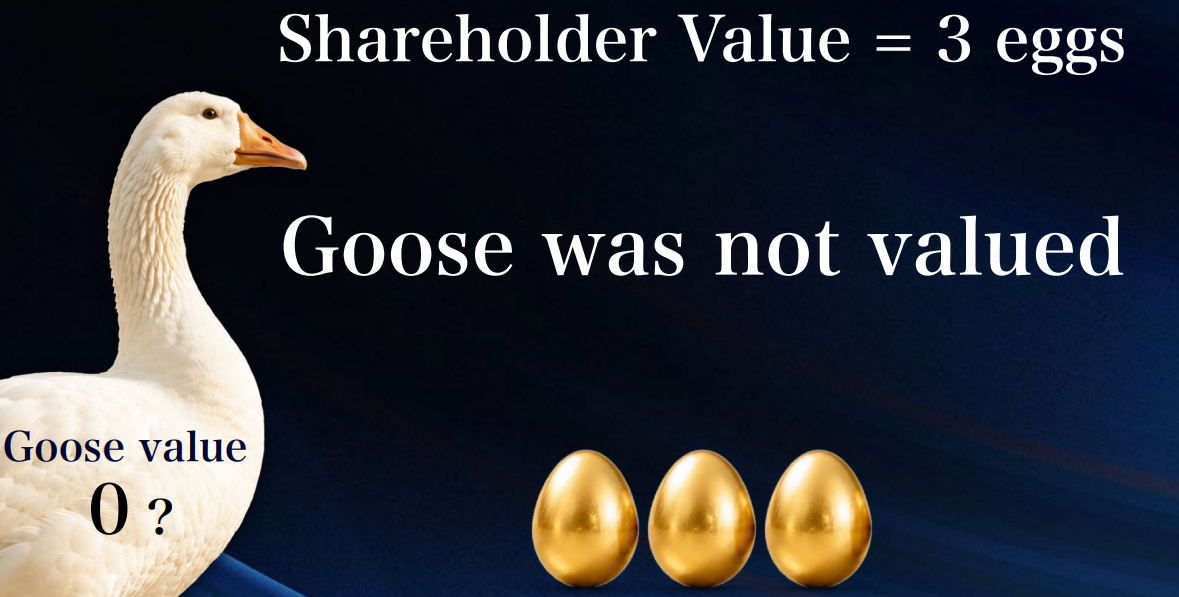

When Masayoshi Son protests that the “goose was not valued,” he’s saying that SoftBank isn’t given its dues for “laying golden eggs,” because the NAV of the company does not give any value to the goose that lays the golden eggs, largely because net asset value refers to the holdings of a fucking company Masayoshi, what are you talking about?

Masayoshi Son’s desperate plea that “what matters is not the eggs, but the goose itself, and its power to keep laying eggs” exists to try and distract from the fact that he’s been pretty bad at fucking the goose for the last decade or so.

The vast majority of SoftBank’s Net Asset Value — which is ¥48.2 trillion rather than ¥74 trillion yen, by the way! — comes from its shares in chip company ARM (¥19.15), SoftBank Vision Fund 1, (¥3.38) and SoftBank Vision Fund 2 (¥17.19). These are two venture capital funds: one very successful (VF1 includes big hits like DoorDash and ByteDance), and one tremendously awful (VF2 includes massive losses on WeWork and Karterra).

His one saving grace, at least on paper, is his early investments in OpenAI, turning around $64 billion (assuming it completes all $30 billion of its 2026 commitments) into a theoretical $100 billion or more, at least if OpenAI goes public, which is almost certain to-

Wait, what was that? OpenAI is leaning toward IPOing in 2027? It hasn’t even held pre-IPO investor meetings or set a timeline? That’s not good at all! The SoftBank Goose Engine only functions if the goose — which was not valued by the way! — continues to lay golden eggs, and in this case, the golden egg is OpenAI, and said egg is still in SoftBank’s ovary!

The problem here is that while SoftBank’s OpenAI stock is “worth $100 billion,” private stock is valued very, very differently to a public stock that you could dump on the market. This is in part because the valuations of private companies are continually overinflated by over-eager investors who, just throwing it out there, might have valued the company based on a belief that they were put on this Earth to create superintelligence rather than whether it was a good business that would continue to grow.

Per the New York Times, OpenAI’s hesitancy to go public came from a concern that it wouldn’t get a value of a trillion dollars — a worrying bit of information considering its was last valued at $765 billion, meaning that advisers were unable to make a convincing case for a listing at a meager 30% premium. This is likely why SoftBank was unable to get a $6 billion margin loan with the entirety of its OpenAI holdings as collateral. Apparently a 6% loan-to-value was too adventurous when it came to stock in what is meant to be the world’s most important company, unless, of course, it isn’t, it won’t be, and its stock is worth fuck all.

Renewed talks for a $10 billion OpenAI-backed margin loan include a guaranteed repayment of the loan if the collateral isn’t able to replace the lost funds, the kind of thing you have to say when the underlying stock ain’t worth nothin’.

OpenAI is Masayoshi Son’s final gambit, as the rest of his endless gambles have gone tits-up at an historic pace. While early bets — like his $20 million investment (around $39 million in today’s money) in Alibaba turning into holdings of over $100 billion (with all of its stock now sold) — have floated the company for years and helped SoftBank recover from the horrors of its dot com bubble collapse,

SoftBank is now horrendously overleveraged across the board, with 85% of its ARM shares and 70% of its SoftBank Corporation tied up in loans, its entire stakes in Alibaba, T-Mobile and NVIDIA liquidated, and the vast majority of its NAV sitting in the deteriorating value of its Vision Fund 1 and its non-OpenAI Vision Fund 2 holdings.

You see, SoftBank is a holding company. It does not have “revenues” or “cashflows” in the traditional sense outside of when it’s able to either sell the things it has or raise debt. As Kakashii put it, Masayoshi Son is a perpetual gambler living in an eternal boom-and-bust cycle, going from losing 96% of his paper wealth after the dot-com bubble burst to sitting at the top of a company with a $200 billion market cap and with golden eggs that are worth, on paper, hundreds of billions of dollars more.

And he’s never, ever gambled more than he has on OpenAI and the greater AI bubble.

While SoftBank’s WeWork washout lost it $16 billion, SoftBank has committed or invested over $60 billion in OpenAI, as well as billions more in related counterprojects like a still-pending 75 billion Euro investment in data centers, its $4 billion acquisition of data center firm DigitalBridge, its $1 billion investment in subsidiary SB Energy to build out more data centers, and its planned $3 billion investment in overhauling a Foxconn plant in Lordstown Ohio.

The future of SoftBank relies on both OpenAI’s ability to go public and maintain a high stock price, as any public offering will likely lead to SoftBank immediately looking for a margin loan. To make matters worse, SoftBank’s other bets hinge upon the continued success of the AI industry, which hinge both on the continued success of OpenAI and there being such incredible demand for AI services (in the hundreds of billions of dollars annually).

And while the geese might have been a clue, SoftBank is a very, very weird company, and the only thing weirder than SoftBank is Masayoshi Son himself.

Yet as goofy and whimsical as this all might seem, SoftBank is also one of the largest companies on the Japanese stock market, valued entirely based on the value of all those golden eggs, and no matter how much value Masayoshi Son might claim his “egg factory” might have, SoftBank’s continued existence relies on its ability to increase its NAV and acquire more debt.

My concerns around SoftBank were well-summarized by The Economist back in May:

Quite how Mr Son will settle these bills puzzles some lenders and frightens others. The cost to insure against a default on its debts has soared. Cashflows from its operating businesses are insufficient. Selling assets would help. But having hawked the family silver (SoftBank sold the last of its Nvidia stock in October), it must now strip metal from the roof of its rusty garage. Its shareholdings in T-Mobile, a telecoms company, Grab, a food-delivery firm, and DiDi, a Chinese ride-hailing platform, are worth much less than they were even a year ago. According to the Financial Times, SoftBank is also considering yet another stockmarket listing, this time made up of an undefined grab bag of loosely AI-related businesses.

The most likely answer is more debt. But from where? The firm already faces a steep wall of maturities: the $40bn bridge loan SoftBank took out to invest in OpenAI matures next March. Selling bonds to Japanese retail investors costs more than it used to. The firm says its level of debt is copacetic, but the “loan-to-value” figure it telegraphs is something of a fantasy, since it ignores an additional $28bn borrowed against stock SoftBank owns in Arm and its Japanese telecoms operation.

It’s unclear what the future looks like for SoftBank. While death is unlikely given its near-systemic presence in the Japanese economy, its continued existence at its current scale is only made possible as long as the world’s most well-funded gambler can keep his seat at the table. While it’s seen boom and bust cycles in the past, SoftBank has never been this levered, and never gambled so hard on a single entity’s success.

While this is technically a company, SoftBank exists and operates at the whim of a man with questionable idols, insane ideas, and fantastical thinking. At one point during the Dot Com Bubble, Masayoshi Son’s net worth was higher than Bill Gates’, rising by more than $10 billion a week, before the majority of his net worth in the space of a year and sending SoftBank’s share price crashing by 93%.

Yet even when adjusted for inflation, SoftBank only invested around $2.93 billion ($1.5 billion at the time) in the heights of Dot Com mania, and spread those investments out over multiple startups.

Today I’m bringing you a guide to one of the silliest companies ever founded, helmed by one of the goofiest men alive, run in a constant state of brittle leverage.

SoftBank only avoided the void in 2023 by dumping its Alibaba shares, and this time around, Masayoshi Son may have gambled too much, putting all of his eggs in one Altman-shaped basket.

Welcome to the Hater’s Guide To SoftBank, or Is Masayoshi Son’s Goose Cooked?