A week ago, analyst TD Cowen revealed that Microsoft had canceled leases "totalling a couple hundred MWs," with "at least two private data center operators across multiple US markets." The report also details how Microsoft "pulled back on converting negotiated and signed Statement[s] of Qualifications (SQQs)," which it added was "the precursor to a data center lease."

Although the analyst added it was unclear whether Microsoft might convert them in the future, these SQQs converted into leases "close to 100%" of the time. Cancelling them was, therefore, rather unusual.

TD Cowen also added that Microsoft was "re-allocating a considerable portion of [its] projected international spend to the US, which suggests to [TD Cowen] a material slowdown in international leasing."

But one crucial, teeny tiny part of the report was missed by just about everybody, emphasis mine:

As we highlighted in our recent takeaways from PTC [Pacific Telecommunications Council conference], we learned via our channel checks that Microsoft 1) walked away from multiple +100MW deals in multiple markets that were in early/mid-stages of negotiations, 2) let +1GW of LOI's on larger footprint sites expire, and 3) walked away from at least five land parcels that it had under contract in multiple Tier 1 markets.

What TD Cowen is saying is not just that "Microsoft canceled some data centers," but that Microsoft also effectively canceled over a gigawatt of data center operations on top of the previously-reported "multiple +100W megawatt deals." If we add in the land under contract, and the deals that were in-flight, the total capacity likely amounts to even more than that.

For some context, Data Center Dynamics reported that Microsoft had 5GW of data center capacity in April 2024, saying that Microsoft had planned to add 1 gigawatt of capacity by October 2024, and another 1.5 gigawatts of capacity by the first half of 2025. Based on this reporting, one can estimate that Microsoft has somewhere between 6 and 7 gigawatts of capacity at this time.

As a result, based on TD Cowen's analysis, Microsoft has, through a combination of canceled leases, pullbacks on Statements of Qualifications, cancellations of land parcels and deliberate expiration of Letters of Intent, effectively abandoned data center expansion equivalent to over 14% of its current capacity.

Sidebar: Let's explain some terms!

Letter of intent — In this context, it’s a statement that an entity intends to lease/buy land or power for a data center. These can be binding or non-binding. A letter of intent is serious — here's a press release between Microsoft and UAE-backed G42 Group signing a letter of intent with the Kenyan government for a "digital ecosystem initiative" (including a geothermal-powered data center) for example — and walking away from one is not something you do idly.

SOQ — Statement of qualifications. These set the terms and conditions of a lease. While they do not themselves constitute a lease, they convert into signed leases at an almost 100% rate (according to TD Cowen), and are generally used as a signal to the landowner to start construction.

Tier 1 market — Essentially, a market for hyperscale growth, helped by favorable conditions (like power, land, cabling). From what I can tell, there's no fixed list of which cities are T1 and which ones aren't, but they include the obvious candidates, like London, Singapore, etc, as well as Northern Virginia, which is the largest hub of data centers in the world.

Megawatt/Gigawatt — This one is important, but also arguably the most confusing. Data center capacity is measured not by the amount of computations the facility can handle, but rather by power capacity. And that makes sense, because power capacity is directly linked to the capabilities of the facility (with more power capacity allowing for more servers, or more power-hungry chips), and because chips themselves are constantly getting faster and more power efficient. If you measured in terms of computations per second, you’d likely have a number that fluctuates as hardware is upgraded and decommissioned. When you read ‘MW/GW’ in this article, assume that we’re talking about capacity and not power generation, unless said otherwise.

These numbers heavily suggest that Microsoft — the biggest purchaser of NVIDIA's GPUs and, according to TD Cowen, "the most active [data center] lessee of capacity in 2023 and 1H24" — does not believe there is future growth in generative AI, nor does it have faith in (nor does it want responsibility for) the future of OpenAI.

Data center buildouts take about three to six years to complete, and the largest hyperscale facilities can easily cost several billion dollars, meaning that these moves are extremely forward-looking. You don’t build a data center for the demand you have now, but for the demand you expect further down the line. This suggests that Microsoft believes its current infrastructure (and its likely scaled-back plans for expansion) will be sufficient for a movement that CEO Satya Nadella called a "golden age for systems" less than a year ago.

To quote TD Cowen again:

"...the magnitude of both potential data center capacity [Microsoft] walked away from and the decision to pullback on land acquisition (which supports core long term capacity growth) in our view indicates the loss of a major demand signal that Microsoft was originally responding to and that we believed the shift in their appetite for capacity is tied to OpenAI."

To explain here, TD Cowen is effectively saying that Microsoft is responding to a "major demand signal" and said "major demand signal" is saying "you do not need more data centers." Said demand signal that Microsoft was responding to, in TD Cowen's words, is its "appetite for capacity" to provide servers to OpenAI, and it seems that said appetite is waning, and Microsoft no longer wants to build out data centers for OpenAI.

The reason I'm writing in such blunt-force terms is that I want to make it clear that Microsoft is effectively cutting its data center expansion by over a gigawatt of capacity, if not more, and it’s impossible to reconcile these cuts with the expectation that generative AI will be a massive, transformative technological phenomenon.

I believe the reason Microsoft is cutting back is that it does not have the appetite to provide further data center expansion for OpenAI, and it’s having doubts about the future of generative AI as a whole. If Microsoft believed there was a massive opportunity in supporting OpenAI's further growth, or that it had "massive demand" for generative AI services, there would be no reason to cancel capacity, let alone cancel such a significant amount.

As an aside: What I am not saying is that Microsoft has “stopped building data centers.” I’ve said it a few times, but these projects take three to six years to complete and are planned far in advance, and Microsoft does have a few big projects in the works. One planned 324MW Microsoft data center in Atlanta is expected to cost $1.8bn and as far as I know, this deal is still in flight.

However (and this was cited separately by TD Cowen), Microsoft has recently paused construction on parts of its $3.3 billion data center campus in Mount Pleasant, Wisconsin. While Microsoft has tried to reassure locals that the first phase of the project was on course to be completed on time, its justification for delaying the rest was to give Microsoft an opportunity to evaluate “[the project’s scope] scope and recent changes in technology and consider how this might impact the design of [its] facilities."

The same Register article adds that “the review process may include the need to negotiate some building permits, potentially placing another hurdle in the way of the project.” The Register did add that Microsoft said it still expected to complete “one hyperscale data center in Mount Pleasant as originally planned,” though its capacity wasn’t available.

These moves also suggest that Microsoft is walking away from building and training further large frontier models, and from supporting doing so for others. Remember, Microsoft has significantly more insight into the current health and growth of generative AI than any other company. As OpenAI's largest backer and infrastructural partner (and the owners of the server architecture where OpenAI trains its ultra-expensive models, not to mention the largest shareholder in OpenAI), Microsoft can see exactly what is (or isn't) coming down the pike, on top of having a view both into the sales of its own generative AI-powered software (such as Microsoft 365 Copilot) and sales of both model services and cloud compute for other models on Microsoft Azure.

In plain English, Microsoft, which arguably has more data than anybody else about the health of the generative AI industry and its potential for growth, has decided that it needs to dramatically slow down its expansion. Expansion which, to hammer the point home, is absolutely necessary for generative AI to continue evolving and expanding.

How Big Is This?

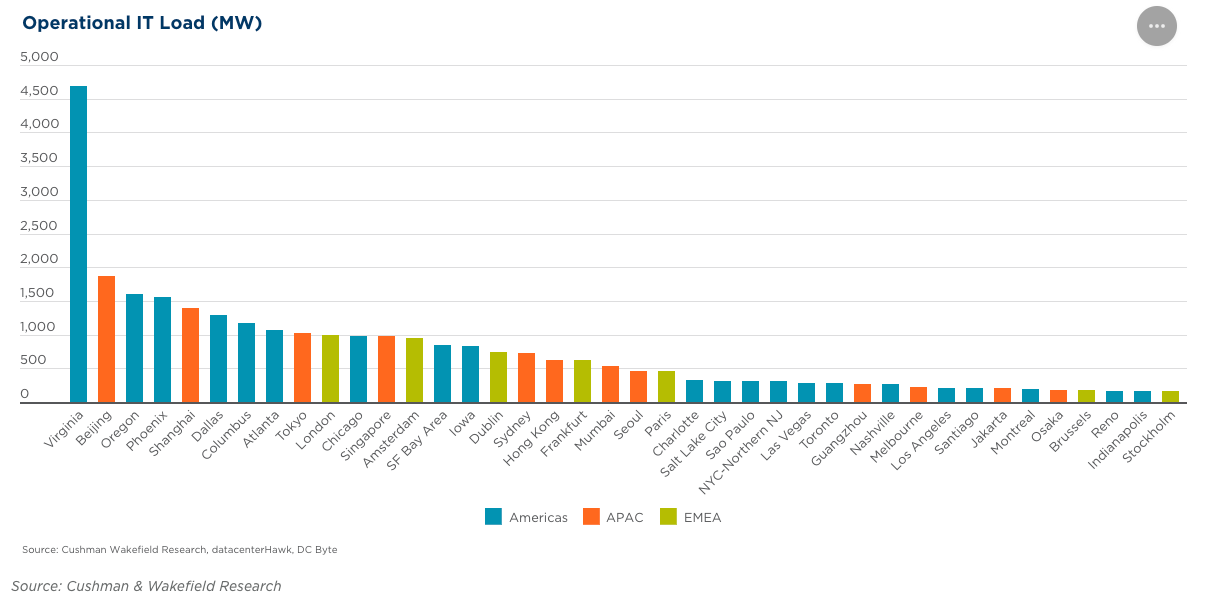

Cushman and Wakefield's 2024 Global Data Center Market Comparison gives some chilling context into how significant Microsoft's pullback is. A gigawatt of data center capacity is roughly the entire operational IT load of Tokyo (1.028GW), orLondon (996MW), or the Bay Area (842MW).

And, again, the total figure is likely far higher than a gigawatt. That number only accounts for the LOIs that Microsoft allowed to expire. It doesn’t include everything else, like the two data centers it already killed, or the land parcels it abandoned, or the deals that were in the early-to-mid stages of negotiation.

Microsoft is not simply "walking back some future plans." It is effectively canceling (what it has loudly insisted is) the future. If you think that sounds hyperbolic, consider this: London and Tokyo are respectively the biggest data center markets in Europe and Asia, according to the same Cushman and Wakefield report.

In the event that Microsoft believed there was meaningful growth in generative AI, it wouldn't be canceling anything, or at the very least wouldn't be canceling so much.

Sidenote: Without context, it’s hard to understand how big a 100MW data center is. These are some of the biggest. According to the International Energy Agency, small data centers can consume anywhere between one and five megawatts. These are, for the most part, average-sized facilities. Perhaps not for cloud computing giants, but for other companies, it’s par for the course.

100MW is, by comparison, huge. It’s the equivalent of the annual energy consumption of between 350,000 and 400,000 electric cars. Although there are others that will likely dwarf what we, today, consider to be a large facility. Meta is in the process of constructing a $10bn data center campus in Louisiana, with a proposed 2GW capacity.

Still, whatever way you cut it, a 100MW facility is a big, long-term investment.

Canceling cities-worth of capacity at a time when artificial intelligence is supposedly revolutionizing everything suggests that artificial intelligence isn't really revolutionizing anything.

One other detail in TD Cowen's report really stood out. While there is a pullback in Microsoft's data center leasing, it’s seen a "commensurate rise in demand from Oracle related to The Stargate Project" — a relatively new partnership of "up to $500 billion" to build massive new data centers for AI, led by SoftBank, and OpenAI, with investment from Oracle and MGX, a $100 billion investment fund backed by the United Arab Emirates. OpenAI has committed $19 billion to the Stargate project — money it doesn't have, meaning that part of $25 billion to $40 billion funding round that OpenAI is currently raising will be committed to funding these data centers (unless, as I'll get to later, OpenAI raises more debt).

Leading the round is SoftBank, which is also committing $19 billion, as well as creating a joint venture called SB OpenAI Japan to offer OpenAI's services to the Japanese market, as well as "spending $3 billion annually to use OpenAI's technology across its group businesses" according to the Wall Street Journal.

In simpler terms, SoftBank is investing as much as $25 billion in OpenAI, then spending another $3 billion a year on software that only loses money, and still hallucinates, and shows no sign of getting meaningfully better or more reliable. Whether Softbank actually sees value in OpenAI’s tech, or whether this purchase deal is a subsidy by the backdoor, is open to debate. Given that $3bn is equivalent to OpenAI’s entire revenue from selling premium access to ChatGPT in 2024 — which included some major deals with the likes of PriceWaterhouseCoopers — I’m inclined to believe the latter. Even then, how feasible is it that SoftBank can continue paying?

To get the deal done, Microsoft changed the terms of its exclusive relationship with OpenAI to allow it to work with Oracle to build out further data centers full of the GPUs necessary to power its unprofitable, unsustainable models. The Oracle/Stargate situation was a direct result — according to reporting from The Information — of OpenAI becoming frustrated with Microsoft for not providing it with servers fast enough, including an allotment of 300,000 of NVIDIA's GB200 chips by the end of 2025.

For what it’s worth, The Wall Street Journal reports that Microsoft was getting increasingly frustrated with OpenAI’s constant demands for more compute. The relationship between the two entities had started to fray, with both sides feeling somewhat aggrieved. This, combined with Microsoft's data center pullback, heavily suggests that Microsoft is no longer interested in being OpenAI's infrastructure partner long-term — after all, if it was, it'd fund and support OpenAI’s expansion rather than doing the literal opposite.

Here's a question: if generative AI had so much demand, why is Microsoft canceling data center contracts? Why is Microsoft — Oracle's largest customer as of the end of 2023 — allowing SoftBank and OpenAI to work with Oracle to build the future rather than itself?

As mentioned previously, TD Cowen specifically noted in its report that Microsoft's "shift in appetite for capacity [was] tied to OpenAI," which heavily suggests that Microsoft is, at best, less invested in the future of OpenAI, a statement confirmed by The Information, which adds that Microsoft had been trying to "lessen its reliance on OpenAI technology as they increasingly compete in selling AI products."

At worst, this situation could suggest that Microsoft is actively dumping OpenAI, and is having questions about the fundamentals of the generative AI industry.

In very plain terms, Microsoft, despite its excitement around artificial intelligence and its dogged insistence that it’s the future of technology, has canceled data center leases and over a gigawatt of other datacenter infrastructure. Doing so heavily suggests that Microsoft does not intend to expand its data center operations, or at least, to the extraordinary levels the company initially promised.

While Microsoft has reiterated that it intends to spend $80 billion in capital expenditures on AI in 2025, it's unclear how it intends to do so if it’s pulling back on data center expansion at such a large scale, and the company has provided no tangible explanation or elaboration as to how it might do so. While hardware upgrades could account for some of its capital expenditures, it would be nowhere near the $80bn figure.

Again, hyperscale datacenters aren’t cheap. They’re massive, billion-dollar (or multi-billion) ventures.

Microsoft also added in a comment to CNBC in the same article that it "[continues] to grow at a record pace to meet customer demand."

Quick question: what customer demand?

Microsoft said back in April 2024 that "AI demand was exceeding supply even after a 79% surge in capital expenditures," and CFO Amy Hood said in its next quarterly earnings in July 2024 that "demand remained higher than [Microsoft's] available capacity." On its most recent (January 2025) earnings call, CFO Amy Hood once said "Azure growth included 13 points from AI services, which grew 157% year over year and was ahead of expectations even as demand continued to be higher than our available capacity."

Riddle me this, Batman — why does a company that keeps talking about having demand that exceeds capacity decide to cancel multiple data centers which, collectively, account for a significant chunk of its existing capacity?

Let's see what Microsoft had to say when asked a week or two ago!

“Thanks to the significant investments we have made up to this point, we are well positioned to meet our current and increasing customer demand,” Microsoft’s spokesperson wrote. “Last year alone, we added more capacity than any prior year in history. While we may strategically pace or adjust our infrastructure in some areas, we will continue to grow strongly in all regions. This allows us to invest and allocate resources to growth areas for our future.”

Sounds like Microsoft built too much capacity, and in fact has yet to see the consumer demand to actually reach it! In fact, a couple of weeks ago Microsoft CEO Satya Nadella said in a podcast interview that "one of the things is that there will be [as a result of data center expansion related to AI] overbuild."

Microsoft also in late January said it had “$13 billion in annual recurring revenue” from AI — not profit, and “AI” is not a line item on its earnings, meaning this is all related revenue put into a ball with no context. Either way, this is a piddly amount that works out to about $3.25 billion a quarter. These are mediocre numbers and Microsoft’s data center pullback suggests that they’re not going to improve.

Sidebar: Now, to be clear, Microsoft, according to CNBC, also leases data center capacity through CoreWeave "and other providers," though at that point the reporters stopped being curious enough to ask "how much" or "who the other providers are." Luckily, with the power of research, I found that The Information reported that Microsoft planned to spend "about $10 billion" renting CoreWeave servers between 2023 and 2030, which is not a particularly high amount when you consider that OpenAI burned 5 billion dollars last year on compute alone. And, as I’ve noted in previous articles, most (if not all) of that spending would be massively discounted, meaning it’s significantly more compute than if, say, you spent $5bn with Azure.

From what I can find, as of the end of 2023 CoreWeave had around $2 billion of revenue contracted for 2024, meaning that $10 billion across seven years would be meaningful revenue for the company, but unlikely to even touch the amount of capacity that Microsoft has cancelled.

According to The Information, OpenAI plans to have Stargate handle three quarters of its computing needs by 2030, which heavily suggests that Microsoft canceling so much capacity is, on some level, linked to OpenAI’s future plans. While The Information reports that OpenAI is still forecasting to spend $13 billion in 2025 and as much as $28 billion in 2028 on Microsoft’s cloud compute, in addition to whatever capacity it gets from Stargate or Oracle, one has to wonder how it intends to do so if it needs the capacity Microsoft simply isn’t building. These are two huge numbers. For context, $13 billion is about ten percent of Microsoft’s cloud revenue in the 2024 fiscal year, though it's unclear whether Microsoft counts OpenAI's compute as revenue.

Nevertheless, I have real concerns about whether OpenAI is even capable of expanding further, starting with a fairly obvious one: its only source of money, SoftBank.

But...what about Stargate?

Let’s start with a few facts:

- Sam Altman’s previous pitch to the Biden administration late last year was that it was necessary to build a 5GW data center.

- We don’t know how big Stargate will be, just that it will initially involve spending $100 billion to “develop data centers for artificial intelligence in the US” according to The Information.

- Stargate’s first (and only) data center deal in Abilene Texas is expected to be operational in mid-2026, though these centers usually become operational in phases. This is especially likely to be the case here, considering that, according to The Information, OpenAI “plans to have access to 1GW of power and hundreds of thousands of GPUs.”

- As part of this, the Stargate Project will construct a 360.5MW natural gas power station. This power station is, as far as I can tell, still in the permitting phase. It’ll be some time before Stargate breaks ground on the facility, let alone starts generating power.

- In the meantime, DataCenterDynamics reports that Stargate has received a permit for onsite diesel generators. These are likely there as an emergency backup (which is normal for data centers), rather than something that would be used while conventional power sources are obtained, as running a hyperscale — or, gigascale — data center with diesel would be insanely expensive. As much as OpenAI and Softbank love to burn money, I think that’s a step too far for them.

- Both OpenAI and SoftBank have committed to putting either $18 billion or $19 billion each — both numbers have been reported.

- OpenAI does not have the money, and is currently trying to raise $40 billion at a $260 billion valuation, with (to quote CNBC) …”part of the funding…expected to be used for OpenAI’s commitment to Stargate.” This round had been previously rumored to value OpenAI at $340 billion, and SoftBank appears to be taking full responsibility for raising the round, including syndicating “as much as $10 billion of the amount,” meaning that it would include a group of other investors. Nevertheless, it certainly seems SoftBank will provide the majority of the capital.

- CNBC also reports that this round will be paid out “over the next 12 to 24 months, with the first payment coming as soon as spring.”

- SoftBank also does not appear to have the money. According to The Information, SoftBank CEO Masayoshi Son is planning to borrow $16 billion to invest in AI, and may borrow another $8 billion next year. The following points are drawn from The Information’s reporting, and I give serious props to Juro Osawa and Cory Weinberg for their work.

- SoftBank currently only has $31 billion in cash on its balance sheet as of December. Its net debt — which, despite what you think, doesn’t measure total debt but rather represents its cash minus any debt liabilities — stands at $29 billion.. They plan to use the loan in question to finance part of their investment in OpenAI and their acquisition of chip design firm Ampere.

- According to SoftBank’s reported assets, their holdings are worth about $219 billion (33.66 trillion yen), including stock in companies like Alibaba and ARM.

- SoftBank has committed to a joint venture called SB OpenAI Japan, and to spend $3 billion a year on OpenAI’s tech.

Doing some napkin maths, here’s what SoftBank has agreed to:

- $18 billion in funding for the Stargate data center project.

- $3 billion a year in spend on OpenAI’s software.

- As much as $25 billion in funding for OpenAI, paid over “12-24 months.” According to The Information, OpenAI has told investors that SoftBank will provide “at least $30 billion of the $40 billion.”

SoftBank made about $12.14 billion (1.83 Trillion Yen) in revenue in Q4 2024, losing $2.449 billion (369.17 billion Yen), but made a profit of about $7.82 billion (1.18 trillion Yen) in Q3 2024.

Nevertheless, SoftBank has agreed to effectively bankroll OpenAI’s future — agreeing to over $46 billion of investments over the next few years — and does not appear to be able to do so without selling its current holdings in valuable companies like ARM or taking on at least $16 billion of debt this year, representing a 55% increase over its current liabilities.

Worse still, thanks to this agreement, OpenAI’s future — both in its ability to expand its infrastructure (which appears to be entirely contingent on the construction of Stargate) and its ability to raise funding — is entirely dependent on SoftBank, which in turn must borrow money to fund it.

On top of that, OpenAI anticipates it will burn as much as $40 billion a year by 2028, and projects to only turn a profit “by the end of the decade after the buildout of Stargate,” which, I add, is almost entirely dependent on SoftBank, which has to take on debt to fund both OpenAI and the project required to (allegedly, theoretically) make OpenAI profitable.

How the fuck does this work?

OpenAI, a company that spent $9 billion to lose $5 billion in 2024, requires so much money to meet its obligations (both to cover its ruinous, unprofitable, unsustainable operations and the $18bn to $19bn it committed to keep growing) that it has to raise more money than any startup has ever raised in history — $40 billion — with the cast-iron guarantee that it will need more money within a year.

To raise said money, the only benefactor willing to provide it (SoftBank) has to borrow money, and is not able to give OpenAI said money up front in part because it does not have it.

SoftBank — on top of the $30 billion of funding and $3 billion a year in revenue it’s committed to OpenAI itself — also has to cough up $18 billion for Stargate, a data center project that OpenAI will run and SoftBank will take financial responsibility for. That’s $48 billion in cash, and $3 billion in revenue, the latter of which, like all of OpenAI’s offerings, loses the company money.

OpenAI has no path to profitability, guaranteeing it will need more cash, and right now — at the time when it needs the most it’s ever needed — SoftBank, the only company willing to provide it, has proven that it will have to go to great lengths to do so. If OpenAI needs $40 billion in 2025, how much will it need in 2026? $50 billion? $100 billion? Where is that money going to come from?

While SoftBank might be able to do this once, what happens when OpenAI needs more money in 6-to-12 months? SoftBank made about $15 billion of profit in the last year on about $46 billion of revenue. $3 billion is an obscene amount to commit to buying OpenAI’s software annually, especially when some of it is allegedly for access to OpenAI’s barely-functional “Operator” and mediocre “Deep Research” products.

As per my previous pieces, I do not see how OpenAI survives, and SoftBank’s involvement only gives me further concern. While SoftBank could theoretically burn its current holdings to fund OpenAI in perpetuity, its ability to do so is cast into doubt by them having to borrow money from other banks to get both this funding round and Stargate done.

Sidenote: On the subject of Softbank’s holdings, I recommend you look at its most recent Group Report. In particular, go to page 29, which lists the ten largest publicly-traded companies in its Vision Fund portfolio. Note how all of them, without exception, trade at a significant fraction of their peak market cap. If Softbank liquidated its assets — and, I admit, this is a big if, and most likely a “worst case scenario” situation — how big would the losses be?

OpenAI burned $5 billion in 2024, a number it’ll likely double in 2025 (remember, the Information reported that OpenAI was projected to spend $13 billion on compute alone with Microsoft in 2025), and it has no path to profitability. SoftBank has already had to borrow to fund this round, and the fact it had to do so suggests its inability to continue supporting OpenAI without accruing further debt.

OpenAI (as a result of Microsoft’s cuts to data center capacity) now only has one real path to expansion once it runs through whatever remaining buildout Microsoft has planned, and that’s Stargate, a project funded by OpenAI’s contribution (which it’s receiving from SoftBank) and SoftBank, which is having to take loans to meet its share.

How does this work, exactly? How does this continue? Do you see anyone else stepping up to fund this? Who else has got $30 billion to throw at this nonsense? While the answer is “Saudi Arabia,” SoftBank CEO Masayoshi Son recently said that he had “not given [Saudi ruler Mohammed Bin Salman] enough return,” adding that he “still owed him.” Nothing about this suggests that Saudi money will follow SoftBank’s in anywhere near the volume necessary. As for the Emiratis, they’re already involved through the MGX fund, and it’s unclear how much more they’d be willing to commit.

No, really, how does this work?

In my opinion, the OpenAI-SoftBank deal is wildly unsustainable, dependent on SoftBank continuing to both raise debt and funnel money directly into a company that burns billions of dollars a year, and is set to only burn more thanks to the arrival of its latest model.

And if it had a huge breakthrough that would change everything, wouldn’t Microsoft want to make sure they’d built the data center capacity to support it?

About GPT-4.5…

Last week, OpenAI launched GPT 4.5, its latest model that…well…Sam Altman says “is the first model that feels like talking to a thoughtful person.” It is not obvious what it does better, or even really what it does, other than Altman says it is “a different kind of intelligence and there’s a magic to it [he hasn’t] felt before.” This was, in Altman’s words, “the good news.”

The bad news was that, and I quote, GPT 4.5 is “...a giant, expensive model,” adding that OpenAI was “out of GPUs,” but proudly declaring that it’d add “tens of thousands of GPUs the next week” to roll it out to OpenAI’s $20-a-month “plus tier” and that he would be adding “hundreds of thousands [of GPUs]” “soon.”

Excited? Well you shouldn’t be. On top of a vague product-set and indeterminately-high compute costs, GPT 4.5 costs an incredible $75 per million input tokens (prompts and data pushed into a model) and $150 per million output tokens (as in the output it creates), or roughly 3,000% more for input tokens and 1,500% more expensive for output tokens than GPT-4o for results OpenAI co-founder Andrej Karpathy described as “a little bit better and…awesome…but also not exactly in ways that are trivial to point to,” and one developer described 4.5 to ArsTechnica as “a lemon” when comparing its reported performance to its price.

ArsTechnica also described GPT-4.5 as “terrible for coding, relatively speaking,” and other tests showed that the model’s performance was either slightly better or slightly worse across the board, with, according to ArsTechnica one “success” metric being that OpenAI found human evaluators "preferred GPT 4.5’s responses over GPT-4o in about 57% of interactions. So, to be crystal clear, the biggest AI company’s latest model appears to be even more ruinously expensive than its last one while providing modest-at-best improvements and performing worse on several benchmarks than competing models.

Despite these piss-poor results, Sam Altman’s reaction is to bring hundreds of thousands of GPUs online as a means of exposing as many people as possible to his mediocre, ultra-expensive model, and the best that Altman has to offer is that this is “...the first time people have been emailing with such passion asking [OpenAI] to promise to never stop offering a specific model.”

Sidenote: As a reminder, GPT-4.5 was meant to be GPT-5, but (according to the Wall Street Journal) continually failed to make a model that “advanced enough to justify the enormous cost,” with a six-month training run costing around $500 million, and GPT 4.5 requiring multiple runs of different sizes. So, yeah, OpenAI spent hundreds of millions of dollars to make this. Great stuff!

This, by the way, is the company that’s about to raise $40 billion led by a Japanese bank that has to go into debt to fund both OpenAI’s operations and the infrastructure necessary for it to grow any further.

Again, Microsoft is cancelling plans to massively expand its data center capacity right at a time when OpenAI just released its most computationally-demanding model ever. How do you reconcile those two things without concluding either that Microsoft expects GPT-4.5 to be a flop, or that it’s simply unwilling to continue bankrolling OpenAI’s continued growth, or that it’s having doubts about the future of generative AI as a whole?

I have been — and remain — hesitant to “call the bubble bursting,” because bubbles do not burst in neat little events.

Nevertheless, my pale horses I’ve predicted in the past were led by one specific call — that a reduction in capital expenditures by a hyperscaler was a sign that things were collapsing. Microsoft walking away from over a Gigawatt of data center plans — equivalent to as much as 14% of its current data center capacity — is a direct sign that it does not believe the growth is there in generative AI, and thus are not building the infrastructure to support it, and indeed may have overbuilt — something that Microsoft CEO Satya Nadella has directly foreshadowed.

The entirety of the tech industry — and the AI bubble — has been built on the assumption that generative AI was the next big growth vehicle for the tech industry, and if Microsoft, the largest purchaser of NVIDIA GPUs and the most aggressive builder of AI infrastructure, is reducing capacity, it heavily suggests that the growth is not there.

Microsoft has, by the looks of things, effectively given up on further data center expansion. At least, at the breakneck pace it once promised.

AI boosters will reply by saying there’s something I don’t know — that in fact Microsoft has some greater strategy, but answer me this: why is Microsoft canceling over a gigawatt of data center expansion? And, again, this is the most conservative estimate. The realistic number is much, much higher.

Do you think it’s because it expects there to be this dramatic demand for their artificial intelligence services? Do you think it’s reducing supply because of all of the demand?

One might argue that Microsoft’s reduction in capacity buildout is just a sign that OpenAI is moving its compute elsewhere, and while that might be true, here’re some questions to ask:

- Microsoft still sells access to OpenAI’s API through Azure. Does it not see the growth in that product to support data center expansion?

- Microsoft still, one would assume, makes money off of OpenAI’s compute expenses, right? Or is that not the case due to the vast (75%) discount that OpenAI gets on using its services?

Microsoft making such a material pullback on data center expansion suggests that the growth in generative AI products, both those run on Microsoft’s servers and those sold as part of Microsoft’s products, do not have the revolutionary growth-trajectory that both CFO Amy Hood and CEO Satya Nadella have been claiming, and this is deeply concerning, while also calling into concern the viability of generative AI as a growth vehicle for any hyperscaler.

If I am correct, Microsoft is walking away from not just the expansion of its current data center operations, but from generative AI writ large. I actually believe it will continue selling this unprofitable, unsustainable software, because the capacity it has right now is more than sufficient to deal with the lack of demand.

It is time for investors and the general public to begin demanding tangible and direct numbers on the revenue and profits related to generative AI, as it is becoming increasingly obvious that the revenues are small and the profits are non-existent. A gigawatt of capacity is huge, and walking away from that much capacity is a direct signal that Microsoft’s long term plans do not include needing a great deal of compute.

One counter could be that it’s waiting for more of the specialized NVIDIA GPUs to arrive, to which the response is “Microsoft still wants to build the capacity so that it has somewhere to put them.” Again, these facilities take anywhere between three and six years to build. Do you really think Blackwell will be delayed that long? NVIDIA committed to a once-a-year cycle for their AI chips after all.

One counter could be that there isn’t the power necessary to power these data centers, and if that’s the case — it isn’t, but let me humour the idea — then the suggestion is that Microsoft is currently changing its entire data center strategy so significantly that it now has to issue over a gigawatt’s worth of statements of intent across the country to different places with…more power?

Another counter is that I’m only talking about leases, and not purchases. In that case, I’ll refer you to this article from CBRE, which provides an elucidating read on how hyperscalers actually invest in data center infrastructure. Leases tend to account for the majority of spending, simply because it’s less risky. A specialist takes care of the tough stuff — like finding a location, buying the land, handling construction — and the hyperscaler isn’t left trying to figure out what to do with the facility when it reaches the end of its useful lifecycle.

Sidenote: I also expect that somebody will chime in and say: “Well, that’s just Microsoft. What about Google, or Amazon?

I’d counter and say that these companies are comparatively less exposed to generative AI than Microsoft. Amazon has invested $8bn in Anthropic, which is a bit less than half Microsoft’s reported investment in OpenAI, which amounted to $14bn as of December. When you consider the discounted Azure rates Microsoft offers to OpenAI, the real number is probably much, much higher.

Google also has a $3bn stake in Anthropic, in addition to its own AI services, like Gemini.

OpenAI, as I also noted in my last newsletter, is pretty much the only real generative AI company with market share and significant revenue — although I, once again, remind you that revenue is not the same as profit. This is true across mobile, web, and likely its APIs, too.

Similarly, nobody has quite pushed generative AI as aggressively as Microsoft, which has introduced it to an overwhelming number of its paid products, hiking prices for consumers as it goes. I suppose you could say that Google has pushed genAI into its workspace products, as well as its search product, but the scale and aggression of Microsoft’s push feels different. That, and it, as mentioned, is the largest purchaser of NVIDIA GPUs, buying nearly twice as many (485,000) as its nearest competitor, Meta, which bought 224,000.

Ultimately, Microsoft has positioned itself at the heart of GenAI, both through its own strategic product decisions, and its partnership with OpenAI. And the fact that it’s now scaling back on the investment required to maintain that momentum is, I believe, significant.

I also recognize that this is kind of a big, juicy steak for someone people call an “AI cynic.”

I have poured over this data repeatedly, and done all I can to find less-convenient conclusions. Letters of Intent are likely the weakest part of the argument — these are serious documents, but not always legally-binding. Neither are SoQs, but as TD Cowen points out, these are treated as the green light to start work on construction, even though a formal lease agreement hasn’t yet been signed. And to be clear, Microsoft let an indeterminate amount of those go too.

Nevertheless, it is incredibly significant that Microsoft is letting so many — the equivalent of as much as 14% of its current data center capacity, at a bare minimum — on top of the “couple hundred” (at least 200) megawatts of data center leases that it’s outright canceled. I do not know why nobody else has done this analysis. I have now read every single piece about the TD Cowen report from every single outlet that covered it. I am astounded by the lack of curiosity as to what “1GW+” means in a report that meaningfully moved markets, as I am equally astounded by the lack of curiosity to contextualize most tech news.

It is as if nobody wants to think about this too hard — that nobody wants to stop the party, to accept what’s been staring us in the face since last year, and when given the most egregious, glaring evidence they must find ways to dismiss it rather than give it the energy it deserves.

Far more resources were dedicated to finding ways to gussy up the releases of Anthropic’s Claude Sonnet 3.7 or OpenAI’s GPT-4.5 than were given to the report from an investment bank’s research wing that the largest spender in generative AI — the largest backer (for now) of OpenAI — is massively reducing its expenditures in the data centers required for the industry (and for OpenAI, a company ostensibly worth at least $157 billion, and which Microsoft owns the largest stake) to expand.

Microsoft’s stake in OpenAI is a bit fuzzy, as OpenAI doesn’t issue traditional equity, and there’s a likelihood it may be diluted as more money comes in. It reportedly owned 49% in 2023. Assuming that’s still the case, are we to believe that Microsoft is willing to strangle an asset worth at least $75bn (several times more than its investment to date) by cancelling a few leases?

How many more alarms do we need to go off before people recognize that something bad is happening? Why is it that tangible, meaningful evidence that we’re in a bubble — and possibly a sign that it has actually popped — is less interesting than the fact that Claude Sonnet 3.7 “can think longer”?

I do not write this newsletter to “be right.” I do not write it to “be a cynic” or “hater.” I write this because I am trying to understand what’s going on, and if I do not do that I will actually go insane. Every time I sit down to write it is because I am trying to understand what it is that’s happening and how I feel about it, and these are the only terms that dictate my newsletter. It just happens that I have stared at the tech industry for too long, and now I can’t look away. Perhaps it is driving me mad, perhaps I am getting smarter, or some combination of the two, but what comes out of it is not driven by wanting to “go viral” or “have a hot take,” because such things suggest that I would write something different if three people read it versus the 57,000 that subscribe.

I am not saying that Microsoft is dying, or making any grandiose claims about what happens next. What I am describing is the material contraction of the largest investor in data centers according to TD Cowen, potentially at a scale that suggests that it has meaningfully reduced its interest in further expansion of data centers writ large.

This is a deeply concerning move, one that suggests that Microsoft does not see enough demand to sustain its current expansions, which has greater ramifications beyond generative AI, because it suggests that there isn’t any other reason for it to expand the means of delivering software. What has Satya Nadella seen? What is Microsoft CFO Amy Hood doing? What is the plan here?

And really, what’s the plan with OpenAI? SoftBank has committed to over $40 billion of costs that it cannot currently afford, taking on as much as $24 billion in debt in the next year to help sustain one more funding round and the construction of data centers for OpenAI, a company that loses money on literally every single customer.

To survive, OpenAI must continue raising more money than any startup has ever raised before, and they are only able to do so from SoftBank, which in turn must take on debt. OpenAI burned $5 billion in 2024, will likely burn $11 billion in 2025, and will continue burning money in perpetuity, and to scale further will require further funding for a data center project funded partially by funding from a company taking on debt to fund them.

And when you put all of this together, all that I can see is a calamity.

Generative AI does not have meaningful mass-market use cases, and while ChatGPT may have 400 million weekly active users, as I described last week, there doesn’t appear to be meaningful consumer adoption outside of ChatGPT, mostly because almost all AI coverage inevitably ends up marketing one company: OpenAI. Argue with me all you want about your personal experiences with ChatGPT, or how you’ve found it personally useful. That doesn’t make it a product with mass-market utility, or enterprise utility, or worth the vast sums of money being ploughed into generative AI.

Worse still, there doesn’t appear to be meaningful revenue. As discussed above, Microsoft claims $13 billion in annual recurring revenue (not profit) on all AI products combined on over $200 billion of capital expenditures since 2023, and no other hyperscaler is willing to break out any AI revenue at all. Not Amazon. Not Meta. Not Google. Nobody.

Where is the growth? Where is all this money going? Why is Microsoft canceling a Gigawatt of data center capacity while telling everybody that it didn’t have enough data centers to handle demand for its AI products?

I suppose there’s one way of looking at it: that Microsoft may currently have a capacity issue, but soon won’t, meaning that further expansion is unnecessary. If that’s the case, it’ll be interesting to see whether their peers follow suit.

Either way, I see nothing that suggests that there’s further growth in generative AI. In fact, I think it’s time for everybody to seriously consider that big tech burned billions of dollars on something that nobody really wanted.

If you read this and scoff — what should I have written about? Anthropic adding a sliding “thinking” bar to a model? GPT-4.5? Who cares! Can you even tell me what it does differently to GPT-4o? Can you explain to me why it matters? Or are you more interested in nakedly-captured imbeciles like Ethan Mollick sweatily oinking about how powerful the latest Large Language Models are to notice the real things happening in the real world with buildings and silicon and actual infrastructure?

Wake the fuck up, everybody! Things are on fire.

I get it. It’s scary to move against the consensus. But people are wondering, right now, why you didn’t write about this, and indeed why you seem more concerned with protecting the current market hype cycle than questioning it.

There are no “phony comforts of being an AI skeptic” — what I am writing about here, as I regularly remind you, is extremely scary stuff.

If I’m right, tech’s only growth story is dead.