When I made my prediction on August 9, I did not expect to be completely right that “SBF’s money is like 400 different loans.” Sam Bankman-Fried did exactly what we feared - he took money from FTX customers’ assets and used it to fund “risky bets by [his] affiliated trading firm Alameda Research.” In plain English, this means that Bankman-Fried took the money that customers put into FTX to trade cryptocurrency (or stocks!) and invested it into a series of loans run by Alameda Research, his other company, to make Sam Bankman-Fried more money. If you’re reading this and saying, “wait, isn’t that illegal?” the answer is “absolutely” - it’s classically known as “fraud” or “theft,” or possibly both.

If you think you’ve heard this story before, it’s because you have - earlier in the year, crypto hedge fund 3 Arrows Capital went under in much the same way:

Except it would appear that the exceedingly rich people behind these DeFi projects are just as reckless and dopey as the people they’re trying to con into using their services. 3 Arrows Capital invested their investors’ funds in other projects to make themselves more money with absolutely no plan for a future where things didn’t go perfectly (including a remarkable $200 million investment in LUNA which is now worth a few hundred dollars), and, of course, not enough money to cover a loss that major. While Celsius may have operated like a bank - investing users’ investments in other investments - they didn’t operate as a bank, making sure that the money they were investing was not money that could be demanded at such a rate that the money simply didn’t exist to return to their customers. And I believe we’re going to see far more of these stories as these networks have the terrible trouble of people asking for their money back.

As I explained on Tuesday, the situation with FTX is both complex and extremely simple - Sam Bankman-Fried is a fraudster that risked customer deposits to enrich himself, and the situation fell apart because Alameda Research, his firm, didn’t have that much money, with most of it locked up in FTT tokens that they could never sell. Since then, Binance walked away from purchasing FTX after doing due diligence, which nobody else appears to have ever done on FTX, and finding a giant hole in the balance sheet.

Alameda Research owes FTX around $10 billion, an eyewatering amount of capital that not even Binance could plug. FTX has halted withdrawals, and that money may be gone. Justin Sun of TRON has said that he will allow anyone with TRON-related tokens (TRX, BTT, JST, SUN, HT) to get them out of FTX using some credit facility, which has given some people hope although I doubt the $10bn hole in FTX is one made up of a significant amount of TRON-related tokens.

If this all sounds like nonsense to you, it’s because it kind of is. Up until this entire crisis, it seemed that Sam Bankman-Fried was the one legitimate guy out of all of them, other than perhaps Brian Armstrong of Coinbase. He was the “newest megadonor that wanted to change Washington,” a CEO that was on a mission to “maximize the total happiness of the future,” leading “effective altruism from a niche movement to a billion-dollar force” - bless his soul, mwah! He shared a “passion for philanthropy” with Gisele Bündchen, and in a podcast from April discussed “taking a high-risk approach to crypto and doing good”:

If you really are trying to maximize your impact, then at what point do you start hitting decreasing marginal returns? Well, in terms of doing good, there’s no such thing: more good is more good. It’s not like you did some good, so good doesn’t matter anymore…

That means that you should be pretty aggressive with what you’re doing, and really trying to hit home runs rather than just have some impact — because the upside is just absolutely enormous.

- Sam Bankman-Fried, April 2022

Bankman-Fried had a nickname: The Prince of Risk, from an article on The Generalist from August 1 2022:

[FTX’s performance] is no mean feat in a sector bloated with wealthy competitors, overrun with hackers and charlatans, and stalked by regulators. To get this far, Bankman-Fried has had to balance peril while moving at speed. He has to interpret and manage risk.

Of course, FTX is far from a sure thing. Few other sectors carry the hazards of crypto, let alone its rate of change. But for now, the company seems to have a suitable leader: a CEO wise to the hazards but willing to step on the gas. It is perhaps an added bonus that in his sleeplessness and idiosyncrasy, Bankman-Fried is an apt avatar for the crypto market in which he operates.

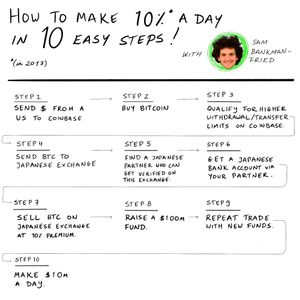

Bankman-Fried’s success allegedly came from arbitrage between the Asian and US cryptocurrency markets, and here’s a very weird diagram of how he allegedly made Alameda Research’s original capital based on an interview with Odd Lots:

However!

While others spotted this inefficiency and sought to capitalize on it, SBF was quick to recognize its limitations. Because the Korean won was a restricted currency, the size of the opportunity was constrained. You could make money, certainly, but deploying hundreds of millions, repeatably, was infeasible. He looked for something bigger.

The “bigger” here was making FTX, the cryptocurrency exchange we all know and love:

The state of the art was poor, SBF felt. In running Alameda, he’d come to appreciate just how much room for improvement there was in the underdeveloped world of crypto. Indeed, despite what Coinbase and others might have marketed at the time, true institutional-grade trading was a ways off, particularly for those interested in more complex securities. BitMEX provided access to derivatives, for example, but like many others, it was prone to outages and other performance issues. With their hands-on experience, SBF felt the Alameda team could create an exchange made for professional investors like them.

If I had to guess, the actual reason that he made FTX was to continue to fund Alameda Research’s operations and generate more capital to gamble with. Perhaps there were noble goals at one point, but the fact that Alameda Research came before FTX heavily suggests that Bankman-Fried wanted to create his own bank. And things only get weirder when you read further in the article (emphasis theirs):

In preparing for this piece, I spoke with someone familiar with both Alameda and FTX’s early days. They highlighted the clear conflict of interest posed by the relationship between the two organizations. Wouldn’t FTX’s exchange favor the market maker founded by its CEO? How could other traders be sure they were receiving a fair shake?

The truth is they may not have. The individual I spoke to explained how vital Alameda had been to FTX initially, providing liquidity for the new market. What’s perhaps less clear is whether Alameda received something in return.

The source noted that FTX drew strong traffic partially because it quoted such tight markets. It seemed impossible to this person that a market maker could actually make money on such spreads, which suggested one of two things were going on: either, Alameda played on a level playing field with others and lost money (essentially subsidizing FTX), or the firm received some kind of advantage. This might have been a first look at the exchange’s trading volume, for example.

…

None of this is illegal, but it’s thorny territory. So far, it has proven worth the risk. SBF has driven both organizations to new peaks. As time passes, Alameda and FTX seem to be growing increasingly independent, perhaps diminishing potential conflicts of interest. But the willingness to operate at the limit of acceptability tells us something about SBF’s orientation and his desire to win, however turbulently.

The sad thing about this piece - published only a few months ago (and a full week before my prediction) - is that it appears to be the only piece of journalism that noticed the issues with Sam’s situation, but, as is the nature of profile pieces, chose to note them and move on. While someone - me, Mario, and I imagine others - might have seen this coming, what possible warning could they have given, and what proof could they have found? What way was there to prove that Bankman-Fried was dipping into client funds, other than that he was completely able to at any time?

As I write this, weird withdrawals are happening from FTX - with concerns that some people close to Bankman-Fried are being allowed to pull their money first. There are no statements from FTX besides Bankman-Fried’s meandering apology and vague hopes of Justin Sun saving somebody. This could be anything - friends of Bankman-Fried, employees at FTX getting their money out while they still can, or technological chaos allowing people who have been randomly mashing the “withdrawal” button to escape with their funds. This may be linked to requirements by the Bahamian regulators (as a reminder, FTX is headquartered in the Bahamas) to get Bahamian funds out of the exchange, but that would involve believing someone that works for FTX.

My general sense is that the FTX situation was caused by 3 Arrows Capital, which in turn revealed Sam Bankman-Fried and Alameda to be screwed in exactly the same way. Alameda had a $500 million loan with Voyager Digital, which caused them to lose enough money that Bankman-Fried transferred at least $4 billion of FTX funds into Alameda’s accounts, including FTT tokens and, somehow, shares in Robinhood, which SBF explained as “rotating a few FTX wallets.” It will take a while to understand exactly how often and in what form Bankman-Fried used FTX funds as collateral, but I would be surprised if this were the only time, and I would imagine there are far more grizzly and egregious things to come out.

Bankman-Fried’s actions call into question every single cryptocurrency billionaire, every specious story about some plucky guy who “hit it big” on Bitcoin, and every muddy tale and rationalization of why someone is allegedly worth so much money now seems utterly disgraceful to believe.

This situation has also shown the cryptocurrency markets to be paper-thin - something that Molly White has written about in detail. People I have talked to have suggested that the cryptocurrency market - with a market capitalization of around $878 billion - only has around $80bn to $100bn of actual, real money. When Bankman-Fried tried to bail out BlockFi and Voyager, he did so by offering (in Voyager’s case) a “credit line” of $200 million “of cash and USDC stablecoins,” as well as a “15,000 Bitcoin revolving credit facility worth approximately $300 million [at the time.]” What’s magical about this is that we have no real insight into how much of this was actual money versus USDC, and while it may have allowed BlockFi to keep working, one has to wonder how it’s possible that BlockFi continues operations if they’re relying on said credit facility. How in the world is that money solvent? How in the world can these companies continue?

The cryptocurrency industry is run on flimflam. There are billions of dollars of trades, but more than half of BTC transactions are fake, meaning that the value of whatever cryptocurrency you’re looking at is manipulated because of the common trading pair of BTC to other cryptocurrencies. The “value” of this industry is entirely specious, derived from people who are intentionally manipulating things to make themselves richer - Bankman-Fried has ties to questionably-collateralized stablecoin Tether, after all.

As a result, any exchange you can think of is at risk of a bank run, except said runs are much worse in cryptocurrency, as the very situation (prices dropping) that causes users to want to withdraw money is one that reduces the value of the assets that the exchange has. While banks are only required to keep 10% of reserves on hand, they also have stringent rules around what they can do with client funds - unlike cryptocurrency exchanges, which can (and likely have) done far worse with your money. Coinbase claims not to do this, and hold funds 1:1, which I genuinely hope is true, but somehow also hasn’t pushed for regulation that makes that a law.

Mark my words; we are not done seeing insane, terrible things happen in this industry. FTX crashed because the cryptocurrency industry had to deal with customers wanting to turn it into real money, and Bankman-Fried’s collapse should make every reasonable-minded person want to remove their money from the ecosystem entirely.

As I’ve previously noted, so much of cryptocurrency is founded upon the belief and trust that your magic beans can be transacted for real money, a test exchanges are beginning to fail. To quote Sam Bankman-Fried in July, more exchanges will fall because “there are companies that are basically too far gone.” And beneath that I have a concern - how stable are the stablecoins? Does USDC really have the money to survive a bank run?

Here’s hoping.

Where’s Your Ed At is a free newsletter, but if you like my work and want to kick me a few dollars, you can do so here.